Vinovest Quarterly Report Q1 2025

The first quarter of 2025 proved dynamic and complex: fine wine prices continued a measured correction even as trading activity climbed, the whiskey market refocused on long-term fundamentals with keen interest in Scotland and Japan, and the entire industry braced for geopolitical headwinds like renewed tariff threats.

Below, we break down how wine, whiskey, and the broader alternative investment landscape fared from January through March 2025.

Further reading

Catch up on last quarter's report here.

By The Numbers

- 1.55% - The average return for Vinovest-managed portfolios in Q1

- -2.1% - The average return for wine on the Liv-ex 1000, an index that tracks 1,000 of the most investment-worthy wines in Q1

- 70% - A surge in price for Bruno Giacosa’s Barolo Riserva 2014 in Q1

Fine Wine Market Performance in Q1 2025

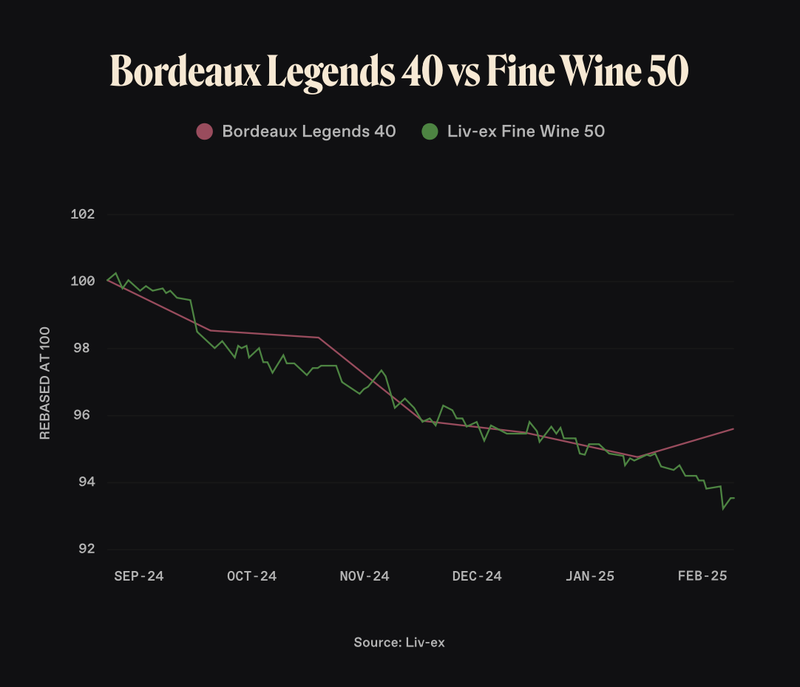

The fine wine market extended its correction in early 2025, but with some intriguing nuances. Liv-ex indices – the benchmarks for secondary market performance – showed continued price softness. The Liv-ex Fine Wine 100 (top 100 wines) declined about 2.0% over Q1 2025, and the broader Liv-ex 1000 (tracking 1,000 wines globally) was down 2.1%. This follows the persistent downward trend observed through 2024, though the pace of decline has moderated. Notably, each major Liv-ex index still fell in March; for example, the Liv-ex 100 slipped 0.7% that month. The bid-offer ratio – a gauge of market sentiment – ticked up by the end of the quarter (0.43 by late March, the highest since January 2024), hinting at a market inching toward stability. In essence, prices are softer, but there are early signs of buyers gradually regaining confidence.

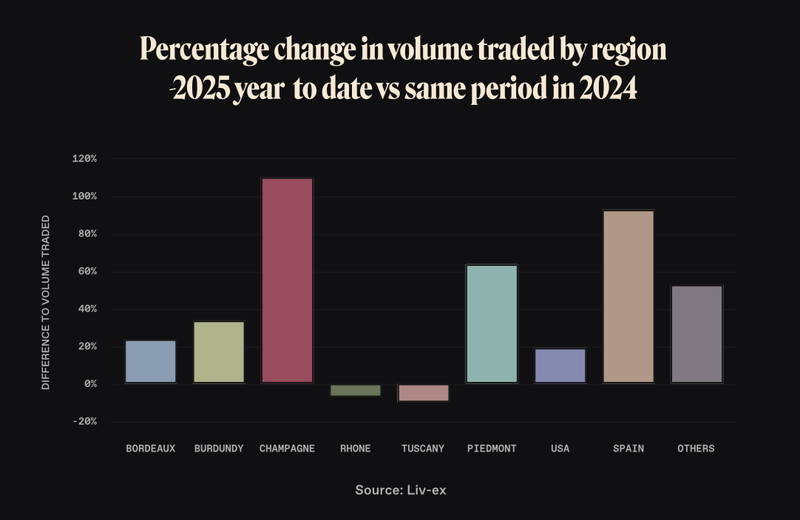

Trading activity painted a more optimistic picture. Despite price declines, Q1 saw robust trading volumes and values on the secondary market. In fact, total trade count, trade volume, and trade value were all higher in Q1 2025 compared to the same period a year prior. March was particularly active: it capped an “active first quarter” with average transaction value in March 2025 rising 2.0% above March 2024’s level. Much of this was driven by high-end Burgundy sales – March saw a surge in Burgundy trading, with volumes up 24% and total Burgundy trade value jumping 39% month-on-month, as buyers seized opportunities in that previously high-flying region. The chart below illustrates the jump in Burgundy’s share of trade by value in March (rising to ~25% of market share from 19% in February) at a time when U.S. buyers pulled back due to tariff concerns:

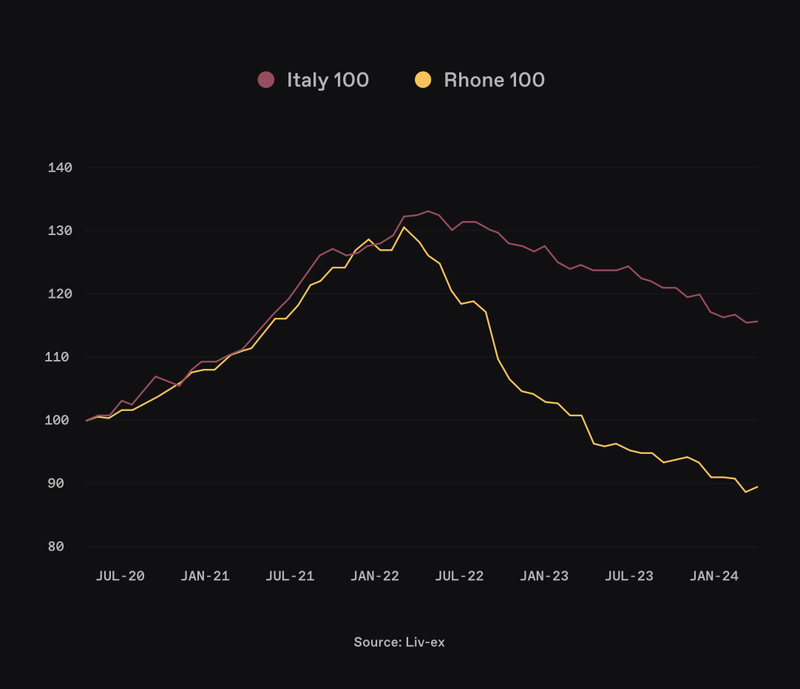

Regional dynamics in Q1 echoed the patterns of late 2024, with a few twists. The two heavyweight regions – Bordeaux and Burgundy – were the weakest performers by price. Each fell roughly 2.9% over the quarter, extending the declines that these markets experienced last year. Bordeaux’s famed First Growths and other blue-chips continued to feel downward price pressure as buyers remained value-sensitive. Burgundy, after its meteoric rise in 2020-2021, also continued a correction, though sustained demand for top Burgundy names remains evident whenever prices dip slightly. By contrast, Italy once again demonstrated resilience. The Liv-ex Italy 100 index was nearly flat (-0.4% in Q1), outpacing other regions. Italian wines – especially Super Tuscans and other marquee labels – have benefited from steady U.S. and global demand, which helped buoy prices. Even as broader indices fell, the Italy 100 sub-index managed a rise of 0.4% in March, underscoring that the market’s interest in Italian fine wine remains strong. Elsewhere, the Rhone region provided a bright spot; after languishing for some time, Rhone wines saw a brief rebound (up ~1.1% in March) as buyers sought value in that category. Champagne, which had been a star performer in recent years, continued to cool off – the Champagne 50 index declined further in early 2025 (it was the worst-performing Liv-ex 1000 sub-index in January), reflecting a normalization after the Champagne frenzy of 2021-2022.

Importantly, even within struggling regions, quality prevailed. Well-regarded wines with strong reputations held firmer on the market. For instance, some Bordeaux châteaux known for consistent quality saw stable or even rising bid-offer ratios despite overall Bordeaux weakness, highlighting how consumer preference for top quality mitigated broad trends. And Q1’s top individual price performers spanned regions: a Châteauneuf-du-Pape from the Rhône (Vieux Télégraphe “La Crau” 2021) spiked +22.7%, a classic Bordeaux second growth (Château Pichon Baron 2013) rose +22.6%, and even a Piedmont gem (Bruno Giacosa’s Barolo Riserva 2014) surged by over 70% off a low base. These outliers aside, the broad strategy for investors remained one of patience. Vinovest’s team continues to emphasize a buy-and-hold philosophy – current trading prices likely reflect short-term liquidity dynamics more than the intrinsic value of the wines.

Whiskey Market Performance

In the world of whiskey, Q1 2025 was a period of consolidation and selective optimism. After the speculative boom and correction of the past couple of years, the market for investment-grade whiskey – particularly Scotch and Japanese whisky – is finding a more stable footing. The final months of 2024 saw a notable correction in American whiskey and oversupplied segments, but by early 2025 the focus had squarely shifted back to the classics: rare single malts from Scotland and prestigious Japanese expressions.

Scottish (Scotch) Whisky: The Scotch whisky investment market remains the cornerstone of whiskey portfolios, and Q1 2025 brought glimmers of a rebound in Scotch demand. Industry reports noted that auction prices for rare single malt Scotch soared in early 2025, with the average hammer price up by double digits year-on-year as compared to Q1 2024 (helped by renewed buying interest from the US and Europe). Investors showed particularly strong appetite for high-end Scotch distilleries like Macallan, Ardbeg, and Dalmore, especially limited releases and older vintages, which continue to command record valuations. This robust bidding activity suggests that the pullback of speculators in 2023 has left a healthier core of serious collectors willing to pay for scarcity and provenance. As one commentator observed, the froth from the pandemic-era whisky flipping has subsided – many quick-profit “flippers” have exited – and what remains is a more sustainable market driven by true enthusiasts and long-term investors. Indeed, the whiskey market’s return to fundamentals is seen as a positive: seasoned collectors and funds are actively picking up blue-chip bottles and casks at what they perceive as value prices after last year’s dip, providing a floor under Scotch prices.

Beyond bottles, whisky cask investment is gaining traction. Q1 saw rising interest in whole cask purchases, as investors seek to capitalize on whiskey’s aging process and potentially higher margins down the road. Several UK and Scottish firms reported increased inquiries for cask ownership programs, reflecting a trend toward longer-term plays in whiskey investing. While casks require patience (and entail storage and insurance costs), they offer the allure of owning appreciating liquid assets that can later be bottled or sold at a premium. This aligns with the broader theme of the quarter: patience and selectivity are replacing the rapid turnover mindset. Overall, sentiment in Scotland’s whiskey market is cautiously optimistic – the consensus is that top-tier Scotch (well-aged single malts from renowned distilleries) should weather economic ups and downs, thanks to global demand from high-net-worth collectors, even if lesser-known or young whiskies face more price volatility.

Japanese Whisky: The Japanese whisky market in Q1 2025 maintained its reputation for excellence, though growth has tempered from its breakneck pace of previous years. Japanese whiskies have been investor darlings for over a decade, fueled by rarity (many aged Japanese expressions are in extremely short supply) and critical acclaim. By late 2024, however, signs of market maturation emerged: after ~15 years of uninterrupted export growth, 2023 saw Japanese whisky export volumes decline by about 9%, the first pullback in recent memory. This cooldown continued into early 2025 as inventory constraints and sky-high prices for marquee bottles (like Yamazaki 18, Hibiki 21, or Karuizawa releases) curbed some of the frenzy. Nonetheless, investor sentiment toward Japanese whisky remained broadly positive. Enthusiasts and funds still avidly pursue iconic bottles at auctions worldwide – the demand for top Japanese labels far exceeds the supply, which has kept prices at lofty levels even if the growth rate of those prices has slowed. In Q1, auction houses reported that Japanese and Taiwanese whiskies continue to command strong interest, often matching or outpacing Scotch in certain sales. In particular, collectors from Asia and the U.S. covet Japanese whisky for its dual appeal as both an investment and a status symbol. Limited-edition releases (e.g. single-cask bottlings from closed distilleries like Karuizawa or Hanyu, or special anniversary editions from Suntory and Nikka) saw lively bidding and in many cases new price highs, underscoring the “holy grail” status that top Japanese whiskies have achieved among connoisseurs.

However, the Japanese segment is not without cautionary notes. The extraordinary appreciation of the past decade – some bottles rose in value hundreds of percent – has made finding “undervalued” opportunities harder. A few high-profile Japanese whiskies actually saw slight price declines from their 2022 peaks as the market digests those gains. Additionally, Japan’s producers have been ramping up capacity (building new distilleries and expanding production) in response to global demand, which in the long run could increase supply. But any such relief is years away from market, so in the near term the rarest Japanese whiskies are likely to remain severely supply-constrained. Investor strategy in Q1 gravitated toward established winners: known-age statement whiskies and historical bottlings, rather than newer, unproven offerings. The travel retail and duty-free channel also started to rebound with the return of global travel in 2025, giving Japanese brands optimism that sales (and by extension brand visibility) will rise in those venues. All told, Japanese whisky continues to be viewed as a top-tier collectible, albeit one transitioning from red-hot growth to a more sustainable trajectory.

Whiskey Market Developments and Outlook: An important development this quarter – though outside Scotland and Japan – was regulatory: the U.S. government officially recognized “American Single Malt” as a whiskey category in January 2025, setting specific standards for its production. This long-sought recognition is a reminder that the whiskey industry globally is evolving, with new categories and regions (from American single malts to emerging Asian distillers) vying for investor attention. For now, Scotch and Japanese whiskies remain the stalwarts of whiskey investment, but the market’s breadth is widening. Q1 also saw some distillery M&A and closures (particularly in the American craft segment) as the industry shakes out excesses. While a few U.S. craft distilleries filed for bankruptcy or closed (citing overexpansion, tariff pressures, and changing consumer habits), the larger trend is one of big players consolidating and new entrants strategizing for premium market share.

For investors focusing on Scotland and Japan, the takeaway from Q1 is clear: quality prevails. The most storied distilleries and age-proven expressions continue to attract a loyal investor base. With the speculative bubble of the pandemic years largely deflated, both the Scotch and Japanese whisky markets are proceeding on a more solid, fundamentals-driven path. This environment rewards deep research and selectivity – exactly the approach that Vinovest’s whiskey team applies when sourcing casks and bottles for our portfolios.

Tariffs and the Q1 2025 Trade Climate

Geopolitical uncertainty cast a long shadow over wine and spirits markets in Q1, with the tariff saga taking center stage. By the end of April 2025, producers and investors were contending with an on-again, off-again tariff situation reminiscent of the turbulence seen a few years ago. The new U.S. administration (in early 2025) rattled markets by threatening and then partially imposing hefty import duties on wines and whiskies – a move that created significant short-term volatility in trading patterns and pricing.

The drama unfolded in several phases. Mid-March 2025 brought the first jolt: the U.S. announced a potential 200% tariff on certain imports, including wine and spirits, as part of a broader trade offensive. Although such an extreme rate was unlikely to materialize fully, the mere threat sent shockwaves through the fine wine market. Almost immediately, U.S. buyers pulled back. Liv-ex data showed that the U.S. share of wine trading by value plummeted in March – falling from about 33% of the market in February to just 21% in March. This 35% relative drop in U.S. buying was “writ large” on the market, resulting in slower bid activity and a notable shift in who was buying: European and Asian buyers stepped in to fill some of the void, often driving bargains as prices softened. The bid:offer ratio on Liv-ex, a measure of demand vs. supply, had just started to improve before the news; after the tariff threat, it remained below the stability threshold of 0.5, reflecting a cautious mood.

Then in early April, the situation took another turn. The U.S. formally imposed a 20% import tariff on European wines (part of a dispute escalation), which took effect briefly – but within days, on April 9th, authorities announced a 90-day pause and reduction of these tariffs. During this grace period (through early July 2025), tariffs on non-Chinese imports were lowered to 10%, giving a temporary reprieve to European wine exporters. This whipsaw policy (tariffs threatened, then applied at 20%, then scaled back to 10%) has left the industry oscillating between fear and relief. As of end of April, the tariff on EU wines into the U.S. stands at 10%, but only temporarily, and the looming possibility of higher rates returning after the 90 days keeps everyone on edge. Market participants widely expect that these next few months will be pivotal – either a resolution will be negotiated to avert the steep tariffs, or the industry will have to adapt to a new normal of pricier transatlantic trade.

The impacts of this tariff turmoil in Q1 were tangible. Wine merchants and investors adopted a defensive posture: many U.S. importers rushed to stockpile wine inventory before tariffs could hit in full, and some European merchants diverted allocations to other markets. (For example, late last year Italian wine exports to the U.S. spiked as merchants shipped early, a trend that likely continued into Q1 2025 in anticipation of tariffs.) On Liv-ex, U.S. bid activity dropped sharply the moment tariffs were on the table – in one 24-hour period (April 2–3), the value of U.S. bids on the exchange collapsed by 80%, as traders recalibrated. Certain regions that rely on U.S. demand, like Bordeaux and Rhône, saw disproportionate declines in American bidding, whereas Burgundy and Champagne – which some European and Asian buyers continued to chase – held relatively more of their U.S. interest. Prices for wines with heavy U.S. exposure came under pressure; sellers in March-April became more willing to accept lower offers, knowing that a key buyer cohort was on the sidelines. As one might expect, trade volume overall didn’t collapse – it actually stayed healthy as other buyers stepped in – but the power dynamic shifted toward a buyer’s market, particularly for U.S.-destined stocks.

The whiskey sector felt the reverberations as well. While the U.S. tariff threats were initially directed at wine, the spirits industry was not far from mind – American officials floated the idea of including spirits, and the EU prepared potential retaliatory tariffs (which could target American whiskey). This isn’t the first tariff rodeo for the whiskey world either: Scotch whisky had been hit with U.S. tariffs in 2019-2020 during a past trade dispute.

Armed with that experience, many whiskey producers took a “forewarned is forearmed” approach. In Q1 2025, Scottish distilleries and Japanese producers largely kept their export strategies steady but cautious – focusing on core markets and ensuring they had contingency plans. Several high-end whiskey brands doubled down on premiumization in domestic markets (aiming to sell the most profitable products at home if export costs spike), and some U.S. importers of Scotch signaled they would reluctantly pass on cost increases to consumers this time, rather than absorb the hit as they did in 2020. The overarching sentiment was frustration and resolve: industry groups like the U.S. Wine Trade Alliance ramped up lobbying efforts, using data from the last tariff episode to argue against self-defeating duties. Even American wine producers joined the chorus opposing tariffs, noting that many supplies they rely on (French oak barrels, glass, etc.) are imported and would get more expensive with broad tariffs.

As of the end of April 2025, the tariff outlook is highly uncertain. The next key date is early July, when the 90-day pause expires – absent a deal, the U.S. could re-impose 20% or higher rates on European wine and possibly spirits. This “Sword of Damocles” scenario has led to hesitant buying patterns: many U.S. wholesalers and retailers are buying just enough to cover near-term demand, wary of being stuck with high-tariff stock, while some overseas suppliers debate adjusting release prices lower to offset potential duties. If tariffs do snap back in full, we could see a more pronounced drop in U.S. wine imports and further price drops on secondary markets as sellers seek non-U.S. buyers. Conversely, if negotiations avert the worst-case tariffs, there may be a relief rally in late Q2 or Q3 as U.S. buyers return vigorously to the market. For now, stakeholders are bracing and adapting. The fine wine market’s correction in Q1 was exacerbated by the tariff specter, but it also underscores the global nature of this asset class – when one major buyer steps out, others (from Europe, UK, and Asia) can step in. Vinovest, for its part, has navigated these conditions by staying diversified (both in client portfolios and geographically in sourcing) and by maintaining a long-term view. As history has shown, policy headwinds like tariffs can cause short-term turbulence yet often prove temporary. The enduring value of great wine and whiskey, by contrast, far outlasts such cycles.

Conclusion

Q1 2025 was a quarter of challenges and opportunities for alternative asset investors in wine and whiskey. Fine wine continued its price correction, with marquee indices down a few percent, but resilient trading volumes and bright spots in regions like Italy indicate that the market’s foundation is sound. Whiskey investments, especially in Scotch and Japanese whisky, proved their staying power – even as the froth from speculative trading receded, the top-tier bottles and casks held investor interest, pointing to a more stable, mature market ahead. Overhanging it all were the twists of geopolitics: the on-off U.S. tariff threats that at times overshadowed fundamentals. By the end of Q1, both wine and whiskey sectors had largely priced in the uncertainty, with participants taking prudent measures to weather potential disruptions.

As we move into Q2 2025, cautious optimism is in the air. Many wealth managers and investors view the current dip in fine wine as an entry point, expecting demand to rise into the latter half of the year. In whiskey, the long-term growth drivers – global passion for premium spirits, finite supply of aged liquids, and innovation in the category – remain firmly in place. While we anticipate continued volatility in the near term (especially around summer when tariff decisions are due), the broader outlook for wine and whiskey investments remains positive. These assets have shown resilience through market cycles, and Q1’s story – of correction, adaptation, and enduring appeal – reinforces why they are invaluable components of a diversified portfolio. Vinovest will continue to monitor these trends closely, deploying our strategy of data-driven insight and expert curation to help our investors capitalize on the opportunities ahead.