Is It Worth Investing In Private Debt In 2025?

Private debt involves investing in debt and benefitting from the repayments. As an alternative investment, private debt has its share of advantages, but there are a few things to keep in mind.

So, what exactly is private debt, and should you invest in it?

In this article, we’ll answer those questions and more, including the various types of private debt, how the private debt market is performing, and some considerations before investing in private debt.

We’ll also examine an excellent alternative (fine wine) and how Vinovest makes investing in fine wine a breeze.

Further reading

- If you'd like to explore more alternative investments, check out the 15 Best Alternative Assets in 2024.

- Considering an art investment? Check out this guide on whether Investing in Art is a Good Idea.

What Is Private Debt?

Private debt, or private credit, is capital invested in debt held by private, often middle market companies. This differs from private equity, which is capital invested in ownership shares of a private company.

Private debt is the third-largest alternative asset class, following private equity and direct real estate.

Private debt isn't traded or issued on the open market, and capital can be loaned to unlisted and listed companies and to tangible assets like real estate.

There are several sources of private debt. While banks participate in private debt, it’s to a lesser extent since the global financial crisis of 2007. As a result, private debt sources include private debt funds, hedge funds, high-yield bonds, collateralized loan obligations, and business development companies.

There are two main categories of private debt:

- Subordinated debt is unsecured, so if there’s a liquidation, holders of subordinated debt will only receive their claims after secured creditors.

- Unsubordinated debt is also known as senior debt. In the capital structure of this debt, a senior secured loan is paid before any other form of debt, reducing the risk involved.

Types Of Private Debt

There are several types of private debt, including:

- Direct lending: Direct lending occurs when senior loans are made directly to middle market companies, i.e., without using an intermediary. Following stricter regulations on banks, hedge funds and institutional private debt managers have played a greater role in direct lending.

- Distressed debt: This is a debt investment made to gain control of a company, usually because of financial distress. Distressed debt usually involves the purchase of securities on the secondary market.

- Infrastructure debt: This is debt used for infrastructure development. Because of the extended life of these assets, the investments generally have a term of 30 years or more.

- Mezzanine debt: Mezzanine debt occurs when a hybrid debt issue is subordinated to another debt issue from the same issuer.

- Real estate debt: Typically, real estate debt refers to direct lending for acquiring real estate. It can include buying and selling securitized real estate loans in the secondary market.

- Special situations: These unusual events compel investors to buy stock, believing its price will rise. It can include trading in the secondary market, direct origination, or distressed debt where the manager thinks price dislocation is present.

- Venture debt: Venture debt is a loan made to early-stage, high-growth companies with venture backing. It’s a short- to medium-term debt financing option to help fund the company’s growth and capital expenses.

The State Of The Private Debt Market

While debt funds can be traced back to the 1990s, they gained popularity after the implementation of new legislation in the wake of the Global Financial Crisis.

Stricter bank regulations meant traditional lenders reducing lending, creating space in the market for lenders like private debt fund managers to offer sources of lending.

This was further supported by milestones in the financial regulatory environment, including the Dodd-Frank Wall Street Reform and Consumer Protection Act and Basel III, have driven demand for financing opportunities from non-bank lenders.

More fund managers began emerging as private debt matured. This increased supply attracted more private equity sponsors.

More recently, alternative investments took a hit from the Covid-19 pandemic. The number of new private debt funds plummeted to a nine-year low, with the amount of new capital raised dropping to a five-year low.

However, Covid led to a wave of distressed debt and special situations funds from private debt investors keen to take advantage of new opportunities. As a result, private debt bounced back and remained stable last year.

Private debt fundraising declined during the pandemic but experienced a swift rebound, thanks partly to an improving economy and liquidity in the credit markets.

Private debt is now a widely accepted investment category. And, since floating rate securities back many private credit funds, private debt investors have certain protections against interest rate uncertainty.

Why Invest In Private Debt?

There are numerous benefits for the private debt investor, including:

- Less risky: Private debt is considered less risky than many other alternative assets and a solid alternative to fixed-income investments.

- Diversification: Additionally, investing in private credit can help create a well diversified portfolio as it’s minimally correlated with public markets, offers a predictable income stream with competitive returns, and is less risky than private equity.

- Popularity: Private debt has become an increasingly popular investment recently. Following improvements in the regulation of banks, a new financial market was created for non-bank entities.

Since there were limited high-yielding opportunities in the public market, investors began exploring the private markets. Private debt funds filled that gap by providing the higher yield investors had been looking for.

- Strong market growth: Low global interest rates have reduced government and corporate bond yields and lowered borrowing costs. As such, investors are now looking for high-yield alternatives to government and corporate bonds while demand for private loans has increased.

Next, consider a few things you should keep in mind before investing in private debt.

What To Consider Before Investing In Private Debt

Although there are some substantial benefits, there are a few things the private debt investor needs to remember before going ahead.

- Illiquid: One of the most significant drawbacks to private credit is the lack of liquidity. Private credit investors must be willing to wait until their investments reach maturity as these instruments are less liquid than broadly syndicated leveraged loans.

- Lack of accessibility: While everyday investors can participate in P2P lending through third-party platforms, many private credit opportunities are only available to the accredited or institutional investor.

- Lower credit quality: Borrowers in this market tend to be smaller with weaker credit profiles. Near the end of 2020, almost 90% of credit estimates were rated ‘b-’ or lower. This increases the risk of default.

- Lack of information: Private debt remains a very relationship-driven investment. With a smaller pool of lenders available, fewer people are aware of the transaction’s details. Additionally, the broad distribution of private loans within lending platforms can make it challenging to accurately track the risk level.

- Reduction in underwriting quality: Strong growth in private debt has reduced underwriting quality. In the broadly syndicated loan market, there’s an increase in EBITDA (earnings before interest, tax, deductions, and amortization) buy-backs as the exact EBITDA definition becomes longer and more opaque.

In other words, companies include more expenses to EBITDA. This makes the profit numbers look better after being adjusted for EBITDA, which is a crucial measure in financing deals.

- No public market: Most private debt investments are made in private markets through unlisted private debt funds. These funds will differ based on their strategy, such as direct lending or fund of funds, and the type of debt provided, such as senior or mezzanine debt.

What’s An Alternative To Private Debt?

If you’re a qualified investor, private debt can form part of a sound investment strategy, offering good diversification with a predictable income stream. Unfortunately, private credit strategies are still largely out of reach for everyday investors.

However, another asset offering strong diversification, with predictable, long-term returns, is available to everyone: fine wine.

Initially, fine wine may not sound like an alternative to private debt, but there are many advantages to investing in a bottle of wine:

- Solid performance: As a luxury collectible, fine wine is often one of the best performers among similar assets, like art, jewelry, and rare whisky. In fact, wine was the top performer in the Knight Frank 2022 Wealth Report, rising 16% throughout the year.

Champagne and Burgundy wines performed particularly well, climbing 31% and 25%, respectively.

- Strong market: Inflation and supply chain concerns continue fuelling demand as people drink more expensive wines at home. This, coupled with an extremely limited supply, bodes well for the wine market.

- Excellent stability: Fine wine is an unusually stable investment. Since it’s minimally correlated with the stock market, it maintains its performance even when stocks are volatile.

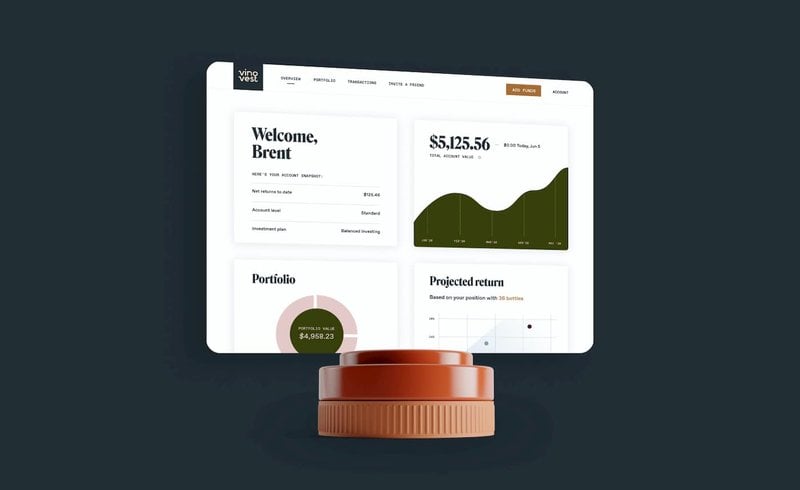

- Accessibility: Once reserved for the accredited and institutional investor,fine wine is now available to everyone. With wine investment companies like Vinovest, you can add this lucrative asset to your portfolio with as little as $1,000.

Vinovest is a prominent wine investment platform that can easily help you buy, store, and sell fine wine from around the world.

Is Private Debt The Right Investment For You?

Private credit strategies can be a solid investment opportunity for a qualified investor. Often considered less risky while providing good diversification with predictable income, it’s a valuable addition to any diversified portfolio.

However, fine wine is an excellent asset for everyday investors that can fit almost any investment strategy. It’s one of the best performers in its asset class with solid growth, long-term returns, and excellent diversification.

Plus, with Vinovest making wine investing easier than ever, what’s not to love?

Simply sign up with the platform and start your wine collection today!