What Is a Retirement Bucket Strategy? (Best Assets to Invest In)

Budgeting for retirement can be overwhelming. You need growing investments and a steady cash flow to fund your retirement expenses.

So, how do you achieve a fine balance between these two goals?

That’s where the retirement bucket strategy comes in. But for it to work, you need to know how to implement it properly.

We’ll shine some light onthis strategy, including how to make it work for you, its main pros and cons, tips, and alternatives to the retirement bucket strategy.

Let’s get started!

Further reading

- Explore other Successful Portfolio Strategies and Tips.

- If you’re an investor interested in alternative assets, check out this In-Depth Guide to some of the Best Alternative Investment Strategies.

What is the Retirement Bucket Strategy?

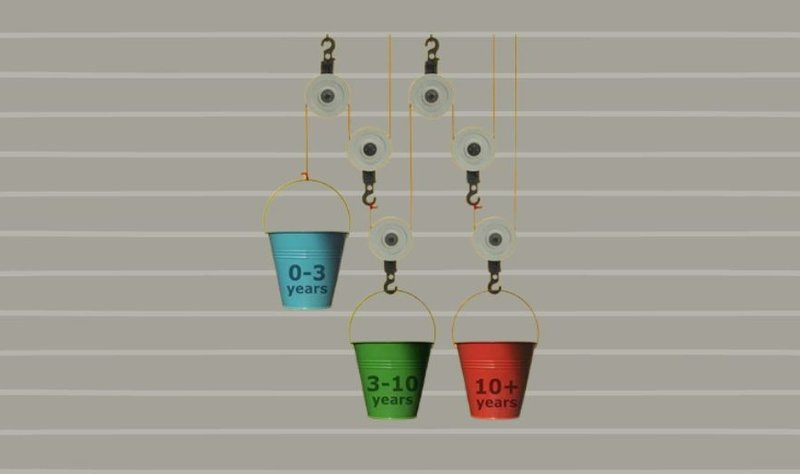

A retirement bucket strategy is an investment approach that distributes your assets into three (or more) buckets.

The assets are divided based on when you’ll need to access them: short-term, mid-term, and long-term.

This retirement income planning strategy was first developed in 1985 by wealth management advisor Harold Evensky. Its core idea was to separate all retirement savings and investments into ‘now vs later’ segments.

This way, retirees can easily access immediate cash while maximizing the gains from long-term investments.

Next, let’s explore how the retirement bucket strategy works.

How to Implement the Retirement Bucket Strategy?

Depending on the financial advisor and their approach, the strategy can be implemented by dividing your assets into three, four, or five buckets.

But most commonly, the assets are divided into three main buckets as follows:

1. Short-Term Bucket

The short-term income bucket includes assets with high liquidity and low yields, such as:

- Cash

- Short-term bond assets

- Short-term CDs

- Saving accounts

- Treasury bills

These assets give you fast access to money. This way, you can cover your immediate income needs and retirement expenses such as monthly bills, living expenses, and emergency needs (home repairs, additional healthcare costs.)

The general recommendation is to have two years of living expenses in this first retirement income bucket.

2. Medium-Term Bucket

This bucket consists of low to medium-risk assets with decent returns (typically, a 5-10% return is expected when there’s low market volatility.) These serve as a fixed income source for years 3-10.

The medium-term retirement assets include:

- Long-term bond and mutual fund assets

- Preferred stocks

- Growth and income funds

- REITs

But you might be wondering:

Are alternative investments a good idea for retirement?

Yes, you can definitely consider investing in alternative investments like fine wine (especially for your mid- and long-term retirement buckets.)

Fine wine, for example, is one of the best performing alternative assets, and in the long term, it has historically outperformed traditional stocks.

For example, the S&P 500’s had a 68% return over the past five years. In contrast, the Champagne 50 index resulted in 93.2% ROI, and the Burgundy 150 was up 121.3% in the past 5 years.

The best part is that you don’t need to be a wine expert or an experienced investor to start investing in this lucrative alternative asset.

If you use the services of Vinovest - a leading wine investment platform, the buying, storing, and selling of wine is taken care of for you. So, you can kick back and enjoy your retirement years while getting all the gains from your wine investments.

3. Long-term Bucket

This bucket contains high-growth, high investment risk retirement assets that you plan to hold for more than 10 years.

But if you want to reduce your vulnerability to stock market volatility, you can add alternative investments like fine wine. This alternative asset class is a good portfolio diversification tool and can fetch enviable returns.

Now:

What are the strengths and weaknesses of this strategy?

Pros and Cons of the Retirement Bucket Strategy

Before you go for this retirement income strategy, consider the following pros and cons:

Pros

The main advantages of the retirement bucket strategy are:

- Security: The strategy provides a certain degree of protection for retirees. If the stock market is down or crashes, you won’t need to sell at a loss. Instead, you will use money from your immediate bucket to cover all your current expenses.

- Structured investment approach: This retirement strategy allows you to plan your retirement income in a structured way, eliminating some guesswork.

Cons

Here are the cons of this retirement withdrawal strategy:

- Asset allocation: Since this retirement planning strategy does not account for exactly how to invest in your buckets and rebalance them, asset allocation and portfolio diversification are neglected.

- Refilling buckets: The strategy does not provide a specific way of refilling your buckets.

This means you might emphasize the short and medium-term buckets and neglect your long-term investments. This can result in your withdrawals outpacing the growth of your long-term investments and diminishing future savings.

To avoid the cons of this strategy, you can consult a certified financial planner or a financial advisor (you can turn to wealth management companies like FMG Suite.)

Retirement Bucket Strategy Tips

Here are a few retirement bucket management tips:

- Rebalancing: The retirement bucket strategy does not advise what assets to hold, at what rate to withdraw them, and how to rebalance your buckets.

That’s why it’s best to apply an additional rebalancing strategy to your bucket strategy. This way, you’ll know when to sell some of your assets to minimize investment risk and optimize your profits.

- Bucket maintenance: When it comes to refilling your buckets, this retirement income strategy can get a bit tricky.

One approach that works in most situations is to use cash holdings and fixed income assets from buckets 1 and 2 (and possibly bucket 3.) Then you should focus on rebalancing your proceeds from bucket 2 and especially bucket 3.

Alternatives to the Retirement Bucket Strategy

If you think the retirement bucket strategy is not suitable for you, consider other retirement planning alternatives like the 4 rule.

Let’s take a look:

- Follow the 4% retirement withdrawal strategy: This systematic withdrawal strategy (also known as the 4 rule) involves withdrawing 4% of your retirement savings in your first year of retirement. In the following years, you keep withdrawing 4% but adjusted to inflation.

- Follow the 45% rule: If you follow this retirement income planning rule, your aim should be to have your retirement savings cover 45% of your pre-tax, pre-retirement annual income. Your Social Security benefits can cover the rest of your income needs.

- Open an IRA or Roth IRA: You can open an individual retirement account (IRA), which offers 401(k) and other benefits. For tax-free retirement withdrawals, consider opening a Roth IRA.

- Delay your Social Security benefits: The Social Security Administration allows you to claim benefits when you turn 62. But you can delay using your Social Security benefits or even decide to work longer.

Plan for a Care-free Retirement Life!

The retirement bucket strategy is a good systematic withdrawal approach you can adopt when entering retirement.

But while it provides good structure, it also requires careful planning on refilling your buckets and allocating tasks. That’s why it’s preferable to work with a professional financial planner if you go for this strategy.

In contrast, you can build your own portfolio of mutual fund assets and alternative investments like fine wine, which have proven to result in stable financial gains in the long term.

To build a successful wine portfolio hassle-free, sign up on Vinovest today!