Vinovest Quarterly Report Q2 2025

Spring into summer 2025 delivered plenty of drama for fine wine and whiskey investors. Fine wine prices continued to grapple with a market correction, with Q2 adding to the declines seen earlier in the year. A mix of external shocks – from tariff threats to currency swings – and internal market dynamics (like an underwhelming Bordeaux en primeur season) kept sentiment cautious. Meanwhile, the whiskey investment arena navigated its own correction, as auction markets recalibrated after a decade-long boom. Yet amidst the challenges, there were pockets of resilience: certain blue-chip wines showed signs of bottoming, Asian buyers began tiptoeing back into the market, and whiskey collectors refocused on quality over speculation. Let’s uncork the details in this Q2 2025 investment report.

Further reading

Catch up on last quarter's report here.

By The Numbers

- 2.85% – The average return for Vinovest-managed portfolios in Q2 (including whiskey returns)

- –4.4% – First-half 2025 change in the Liv-ex Fine Wine 100 index, which fell to 311.6 by end of June. The fine wine benchmark underperformed almost every major asset class year-to-date, reflecting the headwinds facing the wine market.

- –8.8% – Year-to-date change in the Rare Whisky Icon 100 index (top 100 collectible whisky bottles) through mid-2025. After years of gains, rare whisky values have pulled back, illustrating a broader market cooling.

- 11.9% – Increase in fine wine trading volume in H1 2025 versus H2 2024. Trade activity picked up overall, even as prices softened – though nearly 59% of H1’s trade value took place in Q1, before a spring slowdown.

- 55.1% – Growth in Asian fine wine buying by value from H2 2024 to H1 2025. After a long quiet period, Asian buyers are cautiously reemerging – a promising sign for demand, particularly in regions like Burgundy that have caught their focus.

Fine Wine Market Analysis

Index Performance & Market Trends

The fine wine market remained in correction mode through Q2 2025. The Liv-ex Fine Wine 100 – an industry benchmark – lost about 4.4% in the first half of the year. This decline has already exceeded what many expected for the full year. In fact, fine wine has been one of the few asset classes in the red year-to-date, underperforming equities and even most commodities (only crude oil has fared worse). Prices have fallen in 18 of the past 19 months up to June, and the market has not yet found a firm bottom. The Liv-ex 1000 (a broader index of 1000 investment-grade wines) similarly slipped, indicative of widespread softness. Mainstream financial markets, volatile as they were in Q2, managed to regain footing by early summer – but fine wine’s recovery has lagged.

Several acute factors compounded the wine market’s struggles this quarter. Chief among them was the U.S. tariff saga: in mid-March, a threat to impose 200% import tariffs on European wines sent a chill through the industry. Virtually overnight, American buyers – who had been a pillar of support – pulled back from the market. This had an outsized impact on certain segments: U.S. clients had accounted for the lion’s share of trade in some less-liquid regions (like Piedmont, Rhône, and Spanish wines), propping up those markets. Their sudden retreat in Q2 removed that support, accelerating price declines in those corners. The timing couldn’t have been worse, coinciding with Bordeaux’s 2024 en primeur campaign (spring release of the new vintage). Already a tenuous campaign, it proved largely unsuccessful – many major merchants saw lukewarm demand, leaving warehouses brimming with unsold stock. Every tier of the supply chain felt the strain, from châteaux to négociants and merchants. In short, Q2 did not deliver the stabilization that traders had hoped for; uncertainty prevailed.

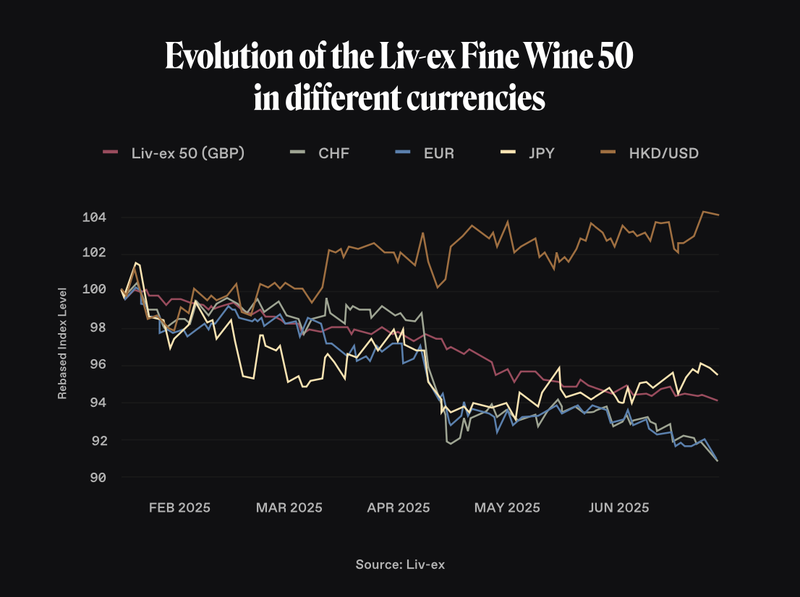

Macroeconomic cross-currents added to the challenge. Currency moves, for example, worked against key buyer groups. The U.S. dollar weakened further against the British pound through Q2, making Bordeaux and Burgundy pricier for dollar-based investors and squeezing arbitrage opportunities. This only reinforced the U.S. buyer pullback. Meanwhile, the euro strengthened against the pound, which fanned the flames in Bordeaux: prices for top Bordeaux wines (often set in euros) looked even less attractive to the trade, forcing deeper discounting to tempt UK and international buyers. The result was a highly cautious market environment.

Regional Highlights: Bordeaux, Italy, Champagne & More

Bordeaux: The biggest name in fine wine is, paradoxically, among the weakest performers this year. The Liv-ex Bordeaux 500 index (tracking 500 leading Bordeaux wines) was the worst-performing sub-index in H1 2025, down 5.6% year-to-date. Prices for younger Bordeaux vintages have been especially hard-hit: it’s become common to see recent vintages (2020, 2021, 2022) trading at all-time lows, often below their original release prices. In contrast, mature Bordeaux has shown more resilience. The Bordeaux Legends 40 index – composed of illustrious older vintages – is only down 2.6% in the same period. These older wines (think renowned 2009s and 2010s) had years to “correct” from any overpricing at release, whereas new releases haven’t had that luxury. This disparity highlights a key theme: ambitious release prices in recent years overshot what the market can bear. Second Growth Bordeaux and other high-tier estates are still trading, but buyers are far more price-sensitive, seeking value and maturity. Technical analysis even suggests that the Legends 40 basket is nearing a support level (its 2011 price peak) and could be bottoming out, whereas the broader Bordeaux 500 may have further to fall absent a demand catalyst. In practical terms, we saw noteworthy price stabilization for some trophy Bordeaux: for example, Château Pétrus 2009 – one of the top performers among legendary wines this year – dipped to around £30,000 per case in April and then rebounded to ~£35,000 (back near its 2018 peak). Such movements indicate that bearish momentum for blue-chip Bordeaux is starting to lose steam, even if a broad recovery remains elusive.

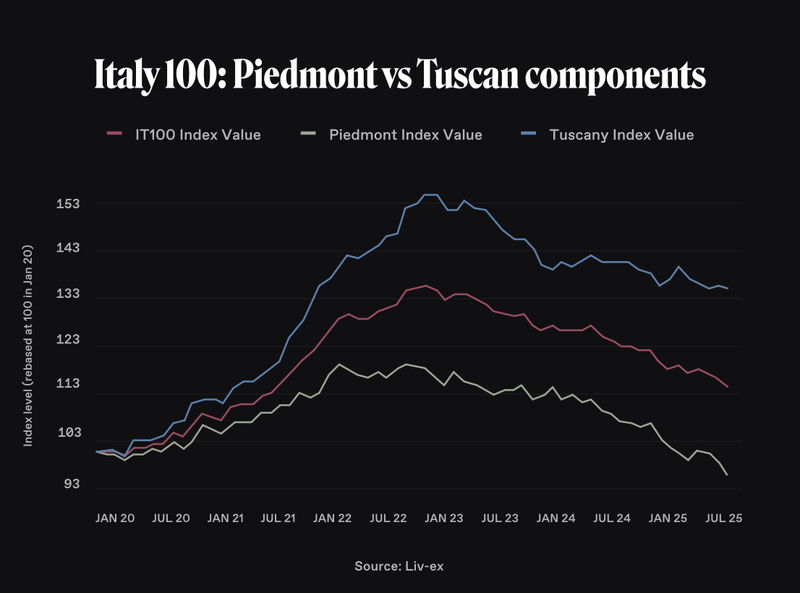

Italy: Italy’s fine wines told a tale of two regions in Q2. Through Q1, the Liv-ex Italy 100 index had been a rare beacon of stability, bucking the broader selling pressure. However, in Q2 the index finally faltered, dropping 3.4% for the quarter. A closer look reveals a stark divergence: Tuscan “Super Tuscans” versus Piedmont’s Barolos. The Tuscan gems (Sassicaia, Tignanello, Ornellaia, Masseto, Solaia, etc.) are down only about 1.3% year-to-date – essentially holding their value. These wines benefit from strong global brand recognition and a broad base of demand.

By contrast, the Piedmontese royalty (Barolo and Barbaresco from producers like Giacomo Conterno, Gaja, Bartolo Mascarello, etc.) are down around 5.6% year-to-date, a sharper drop than the Liv-ex 1000 market average. What explains the gap? One factor is buyer geography: Piedmont wines had become a favorite of U.S. collectors, who accounted for 40%+ of Piedmont trade by value in Q1. When U.S. buying halved in Q2 due to tariff fears, Piedmont prices slid swiftly. Super Tuscans, on the other hand, enjoy more diversified international demand (akin to Bordeaux’s First Growths or Champagne’s Grand Marques), which afforded them some price protection. In short, brand equity matters – and in uncertain times, globally recognized Italian labels held up better than more niche (if equally world-class) Piedmont wines.

Champagne & Other Regions: The Champagne boom of 2020-2022 has definitively fizzled. Champagne was again the hardest-hit region in recent months – the Champagne 50 index fell another 0.7% in May alone, and it remains one of the weakest segments year-to-date. After years of rising prices and intense demand for prestige cuvées, Champagne is undergoing a healthy correction. That said, top Champagne houses (Dom Pérignon, Krug, Salon, etc.) continue to see steady collector interest, and Champagne still accounted for a significant share of secondary market trade (volumes have eased from their peak but are not collapsing). Burgundy, which endured steep price declines over the past year, is showing early signs of life. By the end of Q2 there were reports of Burgundy trade bouncing back, driven partly by renewed Asian buying. The very top Burgundy names – e.g. Domaine de la Romanée-Conti – have seen their prices stabilize as bargain hunters and collectors sense value emerging at the new lower levels. In fact, market chatter suggests savvy buyers are “finding value” in Burgundy’s corrected prices, a notable shift after the region’s sky-high valuations in 2021-22. Beyond Europe, the “Rest of the World” category (led by Napa Valley cult wines) has been a relative bright spot. In the late spring, select back-vintage Californian icons like Screaming Eagle, Opus One, and Dominus saw upticks in demand and even notched some monthly gains, as investors looked outside the traditional regions for growth opportunities. While these pockets of strength haven’t flipped the overall market trend, they underline a key point: even in a down market, quality and rarity find buyers.

Trading Activity & Buyer Behavior

Fine wine trading activity presented a mixed picture. On one hand, trading volumes and values in H1 2025 exceeded late 2024 levels (volume up 11.9%, value up 4.2% vs. H2 2024), indicating sustained interest in wine as an asset class. On the other hand, that activity was front-loaded – fully 58.6% of H1’s trade value took place in Q1, before the tariff scare and market dip in Q2. After mid-April, weekly trading levels fell sharply and struggled to recover. In essence, the tariff turmoil put the brakes on what had been a decent start to the year. Traders became more cautious in Q2, often adopting a wait-and-see approach especially in the U.S.

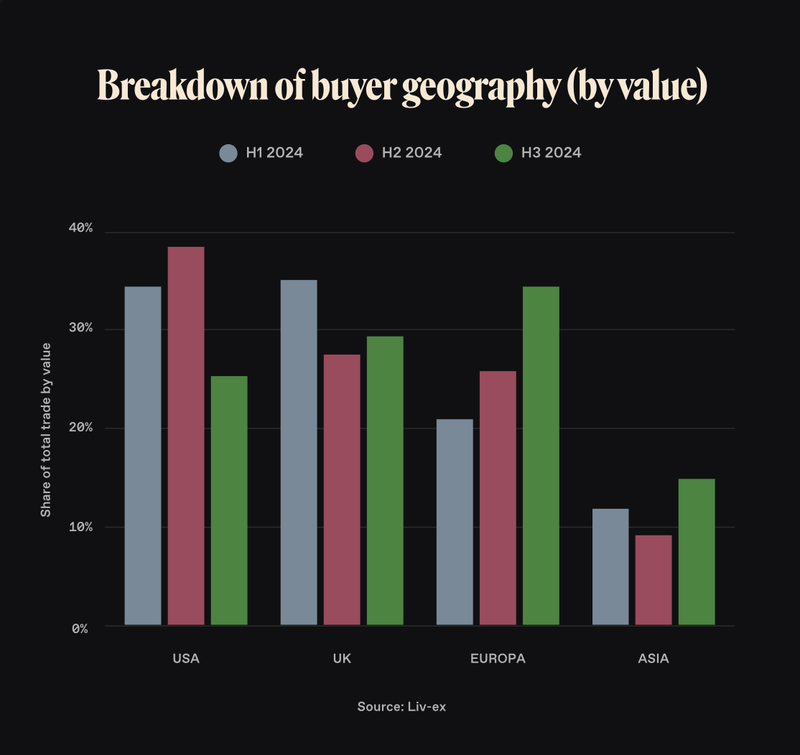

Buyer geography shifted notably this quarter. The U.S., traditionally a powerhouse in fine wine investing, receded to its lowest market share since early 2020. Uncertainty around tariffs and higher costs (exacerbated by a weak dollar) kept American buyers on the sidelines. U.S. merchants and collectors will eventually need to replenish European wine stocks, but few are willing to do so until policy clarity returns. Even if tariffs end up lower than feared, the lack of certainty has imposed a kind of paralysis on U.S. demand.

By contrast, Asian buyers have made a cautious comeback in Q2. After a prolonged lull, Asia’s share of global wine trade is creeping up again – often accounting for around 18% of weekly trade by value in Q2. In nominal terms, Asian spending on fine wine jumped 55% in H1 2025 compared to late 2024. Much of this renewed activity has focused on Burgundy and other cherished regions. It’s a promising development: the market may no longer be able to rely on U.S. participation as it once did, so a re-engaged Asia is welcome news. European buyers remained active as well, though the stronger euro and economic tepidness in some markets limited any big surge from the EU side.

Market sentiment in Q2 was decidedly mixed. There is a growing sense that prices might be nearing a bottom – especially as we see recent vintages trading at rock-bottom levels and older vintages finding support. Indeed, certain 2021 Bordeaux wines (released at lofty prices last year) have now fallen so much that buyers are swooping in, viewing them as bargains. Tellingly, three of the top ten wines traded by value in H1 2025 were Bordeaux 2021s (led by Château Lafite Rothschild 2021). Lafite 2021, for example, was the most-traded wine of the half; after its exorbitant en primeur release at £5,800 per case, it plunged to ~£3,800 and has consolidated around that level. Similarly, heavy trading in Château Mouton Rothschild 2021 and Château Lynch-Bages 2021 suggests that at the right price, demand will readily materialize. These once high-flying young wines have essentially established a new, lower price floor – and buyers are responding, seeing value where a year ago they saw froth. This dynamic gives a glimmer of hope that the broader market downturn can end once prices realign with buyer expectations. Still, confidence remains fragile. Uncertainty is the word of the quarter: uncertainty about tariffs, about the global economy, and about how much farther prices might fall. Until a catalyst arrives – be it a clear tariff resolution, a burst of pent-up demand, or perhaps “fire sale” pricing on oversupplied stocks – the fine wine market is likely to remain in a cautious holding pattern.

Global Whiskey Investment Performance Overview

Market Correction & Trends

The global whiskey investment market in Q2 2025 was characterized by ongoing correction and consolidation. After a decade of phenomenal growth (whiskey was the top-performing “passion asset” of the 2010s, rising ~370% in value over 2013–2021), the past 18–24 months have been a reality check. In the first half of 2025, rare whiskey indices continued to retreat. For example, the Rare Whisky 101 Icon 100 Index – tracking 100 iconic collectible bottles – is down about 8–9% year-to-date. Over a 12-month span it’s off ~14%, reflecting the come-down from the market’s peak. Broadly, prices for high-end scotch have softened across auctions and private sales. The Knight Frank Luxury Investment Index (which famously crowned rare whisky as the best-performing luxury asset for many years) also indicates that whisky’s growth has stalled recently. In short, after years of heady appreciation, the whisky market entered a healthy correction – one that largely persisted through Q2.

Trading data from late 2024 into early 2025 underscores the slowdown. The secondary market for single malt Scotch saw a sharp drop in auction activity in the period covering Q4 2024 through Q1 2025: transaction volumes fell 21% and total value transacted plummeted 53% compared to the same period a year prior. Fewer marquee bottles have been coming to market, and when they do, they often fetch lower prices than a year ago. By Q2 2025, the rate of decline appeared to be moderating somewhat – the market is searching for equilibrium. Interestingly, there are early signs of stabilization: auctioneers report fewer lots going unsold now than in late 2024. This suggests that supply is contracting even faster than demand – sellers are holding back bottles rather than accept fire-sale prices, which in turn is starting to balance the market. Price volatility, while still present, has been concentrated in younger and more plentiful whiskies. Many of the recent price cuts have hit modern bottlings or those with ample supply, whereas ultra-rare historic bottles have seen shallower declines. The market seems to be transitioning from the speculative exuberance of a few years ago to a more selective, value-conscious phase. In this new paradigm, brand strength, rarity, and provenance are paramount – bottles from distilleries with sterling reputations (and genuinely scarce releases) continue to hold investors’ interest and should better retain value.

A noteworthy development in Q2 was the continued retreat of the ultra-premium segment. The frenzy for $30,000+ bottles has cooled markedly. In fact, sales of super-expensive bottles (above ~£10,000 each) have become infrequent, revealing a shift in collector behavior. Top-end buyers either stepped back from bidding wars or decided to hold their treasures rather than consign them into a weak market. This led to a significant contraction in the premium tier of the market. By contrast, mid-tier and lower-value whiskies now dominate both the volume and value of sales. More collectors are focusing on attainable gems and overlooked distilleries, hunting for relative bargains. In essence, the market has broadened out: instead of just a few trophy bottles garnering all the attention, a wider array of whiskies is trading hands, but at lower price points. This democratization is not necessarily a bad thing – it signals that the whisky market is maturing and perhaps becoming less bubble-prone at the top.

Notable Labels, Trends & Structural Shifts

Even in a down market, certain “hero” labels in the whiskey world continue to stand out – notably Macallan. The Macallan remains the quintessential blue-chip whisky brand, accounting for an outsize share of auction market value (around 40% by some estimates). Its dominance was evident again this year: multiple Macallan bottlings still rank among the most sought-after and highly valued. In fact, in the eyes of many collectors, Macallan is a bellwether for the whole whisky sector. Recent reports noted that five of the top six auction price spots in late 2024/early 2025 were held by Macallan releases – including legendary bottles like the Macallan 60-Year in Lalique and the Macallan “Red Collection” editions. These ultra-rare Macallans, often selling well into five figures, underscore that the very top of the market can still command enthusiasm, albeit with fewer trades. Outside of Macallan, other iconic distilleries like Springbank, Bowmore, and Ardbeg remained highly collectible and actually gained relative share of investor interest as Macallan’s lead narrowed slightly. Notably, Springbank – a cult Campbeltown distillery – has seen such fervent demand that some of its limited releases now rival Macallan in auction performance.

Japanese whiskies (e.g. Karuizawa, Yamazaki) also continue to be prized, though their market has cooled from the peak frenzy of a few years ago. In short, whiskey investors are still chasing the best of the best – but they are doing so more selectively, and record-shattering bids are rarer in 2025 than during the last boom.

For whiskey as an asset, structural trends in Q2 2025 are worth noting. One positive development is on the regulatory front: the UK moved to ease the trading of maturing whisky casks, bringing rules closer to those for wine trading. Effective March 2025, HMRC updated WOWGR regulations so that storing and trading whisky casks in bond is simpler and more transparent, similar to how fine wine is handled. This is expected to boost the nascent whisky cask investment market by lowering logistical barriers. Indeed, barrel investment has been a growing trend – platforms (including Vinovest itself) have facilitated purchases of young casks with the promise of future returns as the spirit ages. Investors should remember, though, that casks are long-term holds: whisky matures over many years, and the “angel’s share” (evaporation) slowly shrinks the volume (about 2% loss per year).

In terms of investor sentiment, whiskey stakeholders in Q2 2025 were generally patient and strategic. There’s a growing recognition that the easy money of the last decade – when virtually any aged single malt would rise in value – has given way to a more discerning market. The advice du jour is to focus on quality: top distilleries, limited releases, and bottles with impeccable provenance. The market’s transition “from speculative exuberance to selective, value-conscious buying” is ultimately a healthy evolution. It suggests that whiskey investing is professionalizing, with collectors doing deeper research and looking at long-term fundamentals (age, rarity, distillery reputation) rather than chasing hype. To wit, a recent expert panel identified several “undervalued” rare whiskies for 2025 – signaling that there are perceived bargains out there after the price corrections. And despite the near-term dip, the long-run case for whiskey remains intact: consumer demand for premium spirits keeps growing globally, and the supply of truly great, aged whisky will always be finite. Indeed, over a 10-year view, rare whisky still leads virtually all alternative assets in performance. This quarter’s cooler market may well be an attractive entry point for investors with a contrarian bent and a bit of patience.

Outlook for H2 2025 and Beyond

As we enter the second half of 2025, both the fine wine and whiskey markets find themselves at inflection points. Fine wine is tantalizingly close to a potential bottom – yet not quite out of the woods. Prices have come down to levels where value-oriented buyers are nibbling, as evidenced by the trading in undervalued recent vintages. If the market is to turn the corner in H2, a few things likely need to happen: First, a resolution (or at least clarity) on the U.S. tariff issue is essential. The latest news in early July indicated some progress in negotiations, which provided a ray of hope. Ultimately, even if tariffs land on the higher side, certainty will allow the trade to adjust margins and move forward. Second, a shift in overall market sentiment is needed – a spark to encourage buyers that it’s safe to re-enter in force. That catalyst could come in the form of a strong resurgence of Asian demand (if, for example, China’s economic outlook improves or its appetite for wine fully returns). It could also come from within the industry: we might see merchants running clearance sales on oversupplied stocks, effectively resetting prices to levels that attract a new wave of collectors. Liv-ex analysts note that as the market grinds lower, we are “getting closer to the floor” – and history shows that once a floor is found, recovery can build quietly and then quickly. For now, expectations for H2 are cautious. The trade has tempered its optimism after a disappointing Q2. But there is underlying confidence that fine wine’s fundamental appeal – tangible assets with limited supply and global demand – remains sound. Long-term investors may view this period as an opportunity to acquire blue-chip labels at a relative discount, positioning for future gains when the cycle turns up again.

For whiskey, the outlook is one of guarded optimism and disciplined strategy. The recent market correction, while painful for some, has likely purged a degree of speculation and froth. As the whisky market transitions to a more stable footing, H2 2025 may bring a gradual return to modest growth, especially for the most distinguished bottles and casks. We expect to see the high-end auction segment pick up if sellers feel pricing has stabilized – a few headline-grabbing sales of rare old Scotch (think Macallan or Dalmore decades-old releases) could signal renewed confidence. Until then, the action will center on the mid-market: collectors trading into names like Springbank, Ardbeg, and well-regarded independent bottlings that offer rarity without a stratospheric price tag. The whiskey cask investment space should also continue to develop, aided by regulatory improvements and growing awareness. Vinovest and other platforms have now built a two-year track record with whiskey, and if they can showcase consistent positive returns (like the cask revaluation gains seen this quarter), more investors may be enticed to allocate funds into maturing spirits as a complement to their wine holdings.

In sum, Q2 2025 reminded investors that even passion assets like wine and whiskey are not immune to broader market forces and cycles. After a frothy few years, both markets are normalizing. Fine wine is searching for its bottom – but with every tick down, it inches closer to recovery, especially as savvy buyers swoop in on quality names at value prices. Whiskey is emerging from a much-needed cooldown, with a smarter, more selective marketplace taking shape. For investors, the key in the coming months will be selectivity and patience. Those who can identify the over-corrected gems – be it a First Growth Bordeaux from an unloved vintage, or a top-tier single malt distillery’s limited release that got caught in the downturn – may reap the rewards when the pendulum swings back. The long-term drivers for both wine and whiskey (growing global affluence, expanding collector bases, and finite supply of the best products) are intact. As always, a balanced portfolio and a keen eye on market signals are advised. We at Vinovest remain committed to navigating these shifts with you – finding opportunity in the midst of uncertainty, and toasting to the eventual upturn when the time is right.