Money Market Funds: How They Work, 10 Best Options, & Alternatives

Money market funds were introduced in the 1970s and have been popular ever since. They have low volatility and tend to be highly liquid.

Interestingly, money market fund assets in the US are currently valued at $4.67 trillion.

But what are money market funds, and how do they work?

Let’s explore everything about these funds — how they operate, how to invest in them, the various money market funds to invest in, their pros and cons, and more.

We'll also check out an ideal alternative investment (fine wine) that offers lucrative returns.

Further reading

Check out our guide that covers everything about Alternative Investment Funds.

And if you want to discover tips on investing in a profitable asset like wine, check out this Fine Wine Investment Guide.

What Is a Money Market Fund?

A money market fund is a fixed mutual fund that invests in short-term debt securities with minimal credit risk.

Money market funds have low risk, a short maturation period, and can be tax-exempt depending on the type of securities they invest in.

Although a money market fund is usually mistaken for a money market account, these two are different. A money market account is a personal savings account, while a money market fund is a fixed income mutual fund.

How Do Money Market Funds Work?

Money market funds operate like any other mutual fund. They issue shares to an institutional or individual investor, and follow the guidelines set by the Securities Exchange Commission (SEC).

The return on investment (ROI) of these funds depends mainly on the interest rates.

Money market funds invest in debt-based securities such as:

- Commercial paper: Short-term corporate debt.

- Certificate of deposits: Bank-issued savings certificates with a short maturity date.

- Banker's acceptances: Short-term debt or payment guaranteed by a commercial bank.

- Repurchase agreement: A short-term agreement where an individual or government agency sells securities and repurchases them later at a slightly higher price.

Money market funds usually aim to maintain a net asset value (NAV) of $1 per share. The excess earnings generated from these funds are distributed to individual and institutional investors through dividend payments.

Occasionally, the net asset value of a fund may fall below the $1 NAV and create a condition called "breaking the buck." This condition usually causes temporary price fluctuations in the money markets.

If the “breaking the buck” condition continues, it may cause the money market fund’s investment income to be less than its operating expenses or investment losses.

Money market funds must hold at least 10% of their total assets in daily liquid assets, and at least 30% in weekly liquid assets.

The SEC regularly issues a press release on money market fund reform — a set of rules that address any potential financial instability caused by money market funds.

The most recent money market fund reform includes changes to swing pricing policies and the Form N CR reporting documentation.

Swing pricing refers to adjusting the fund’s price above or below its NAV value. Meanwhile, Form N CR is used for reporting the income generated from money market funds.

According to the SEC, tax-exempt money market funds should apply relevant swing pricing policies and adjust the NAV per share when the fund experiences net redemptions (the state where there’s more money flowing out of a mutual fund and less money flowing in).

But how do you put money into a money market fund?

You can invest in money market funds by:

- Contacting a fund provider like Fidelity or Vanguard

- Buying money market funds through a bank

- Purchasing through a traditional or Roth IRA as part of a retirement strategy

- Seek the help of a financial professional who can help you pick the best option

Now, let’s check out how money market funds are structured.

4 Types of Money Market Funds

Money market funds come in different forms depending on the maturity period and the assets within the fund.

Here are some money market funds to choose from:

- Prime Money Fund: A prime money market fund invests in commercial paper of non Treasury securities issued by a government agency, a government-sponsored enterprise, or corporations.

- Government Money Fund: This money fund invests almost all its assets in government security, cash, and a repurchase agreement that is fully collateralized by government security or cash.

- Treasury Fund:The fund invests in debt security issued by the US Treasury, such as Treasury bills, Treasury notes, and Treasury securities.

- Tax-Exempt Money Fund: A tax-exempt money fund (such as a municipal bond) provides individual and institutional investors with returns free from the federal reserve income tax.

But how do you pick the right money market fund?

3 Ways to Choose a Money Market Fund to Invest In

Here’s how you can add a suitable money market fund to your portfolio:

- Decide if a Money Market Fund Is Right for You

- Explore Different Money Market Funds

- Compare Different Money Market Funds

1. Decide if a Money Market Fund Is Right for You

Before investing in a money market mutual fund, make sure it aligns with your investment objective.

Although money market funds usually earn a stable interest rate over time, the withdrawal process is more complex than visiting your bank. If you need the funds, you'll have to write a large check or electronically transfer them.

So, this means money market funds might not be the right choice if you’ll need the money quickly.

Also, money market funds are not insured by the Federal Deposit Insurance Corporation. This means the government won’t insure the funds if the investment firm that provides your money market fund defaults.

Generally, money market funds are suitable for an individual investor with a short-term investment objective, or investors who want to diversify their portfolio holdings with low-volatility assets.

2. Explore Different Money Market Funds

Money market funds are available through various institutional funds, including Vanguard and Charles Schwab. They offer a range of funds with varying risks and investment returns.

Explore these money market funds by visiting their websites or popular sites like Yahoo Finance. Also, contact a financial professional to discover the money market funds they offer.

3. Compare Different Money Market Funds

Whether you’re an institutional or individual investor, you’ll have to assess different funds carefully. Request fund documents such as the prospectus and the Form N MFP for various retail and institutional funds.

The prospectus outlines how each fund operates and the types of securities it invests in. Meanwhile, Form N MFP is a monthly report of the fund's activities.

Investment companies usually produce monthly and annual reports displaying the performance of their funds. These reports also include Key Investor Information Documents (KIIDs) and a summary prospectus that provides insight into the fund’s structure and performance.

Here are the other things to look out for when comparing money market funds:

- The tax status of each fund: Taxable money market funds usually offer a higher yield than their tax-free counterparts.

- Overall expenses: Most funds have a variety of charges, such as a sales charge, management fee, and liquidity fee. These fees can seriously diminish your returns in the long run.

- Yield history: The yield for different money market funds fluctuates from time to time. So, it’s important to examine each fund's current yield and its yield history. Keep an eye out for the expense ratio and daily liquid assets to gauge expected investment returns.

- Credit ratings: The credit ratings of the security held by a fund can help you gauge the credit risk of each fund. So, always check the credit rating before picking a money market fund.

Let’s now discover the best money market funds that deserve a spot in your portfolio holdings.

The 10 Best Money Market Funds to Invest In

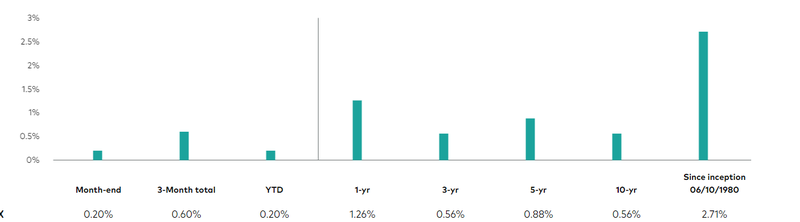

- Vanguard Municipal Money Market Fund

(Minimum Investment: $3,000, 7-day yield: 2.36%)

- Schwab Municipal Money Fund

(Minimum Investment: $0, 7-day yield 2.04%)

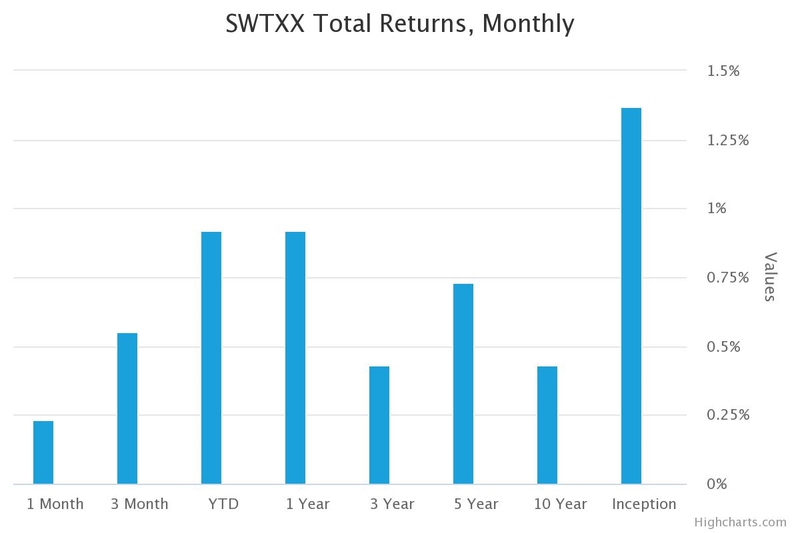

- Fidelity Investments Money Market Fund

(Minimum Investment: $1,000,000, 7-day yield: 3.76%)

- Schwab California Municipal Money Fund

(Minimum Investment: $0, 7-day yield: 1.87%)

- Fidelity Municipal Money Market Fund

(Minimum Investment: $0, 7-day yield: 1.63%)

- Federated Hermes Tax-Free Obligations Fund

(Minimum Investment: $500,000, 7-day yield: 1.67%)

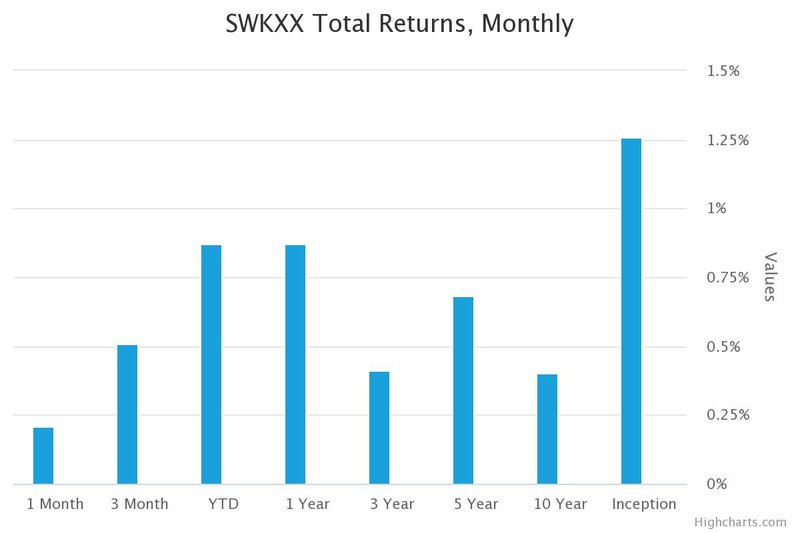

- BlackRock Liquidity Funds MuniCash

(Minimum Investment: $5,000, 7-day yield: 1.53%)

- Federated Hermes Municipal Obligations Fund

(Minimum Investment: $500,000, 7-day yield: 1.84%)

- Dreyfus National Municipal Money Market Fund

(Minimum Investment: $2,500, 7-day yield: 0.00%)

- Fidelity New York AMT Tax-Free Money Market Fund

(Minimum Investment: $25,000, 7-day yield: 1.70%)

Now, let’s check if it’s worth investing in these funds.

Are Money Market Funds a Good Investment?

Here are the pros and cons of investing in money market funds:

Advantages of Money Market Funds

- Low volatility: Money market funds are one of the most stable and least volatile mutual funds.

- High liquidity: You can easily retrieve or transfer funds from a money market mutual fund to other investments. The process typically takes one business day.

- Security and Stability: Federal regulations require that money market mutual funds invest exclusively in low-risk, short-maturity securities. This makes these investment funds less susceptible to market fluctuations.

- Lucrative tax advantages: Some money market funds invest in assets whose interest payments are exempt from taxes. These funds can provide you with stable tax-free earnings.

Disadvantages of Money Market Funds

- Lack of insurance: Since the Federal Deposit Insurance Corporation doesn’t insure money market funds, there’s a risk that you may not receive a $1 per share value when you redeem your shares.

- Price fluctuations: The share price of a fund fluctuates. So, this means when it’s time to sell your shares, there’s a possibility they’ll be worth less than what you originally paid.

- Foreign exposure: The ROI for Money market funds from other countries is susceptible to political, economic, and regulatory changes in those foreign countries.

- Susceptible to market conditions: Money market mutual funds typically invest in assets of short-term nature. The funds may not be the right choice if you're looking for investments to hedge against market conditions like inflation.

- Potential lack of liquidity: If the liquidity of a money market fund falls below the required minimums, this could temporarily limit your ability to sell shares.

Let’s face it — investing in money market funds might not always be worth it. In fact, the entire process can be pretty complicated.

Instead,you could check out another lucrative alternative asset like fine wine!

Fine Wine: A Stable, High Return Asset

Investing in fine wine is a profitable and hassle-free way to diversify your portfolio holdings.

Why?

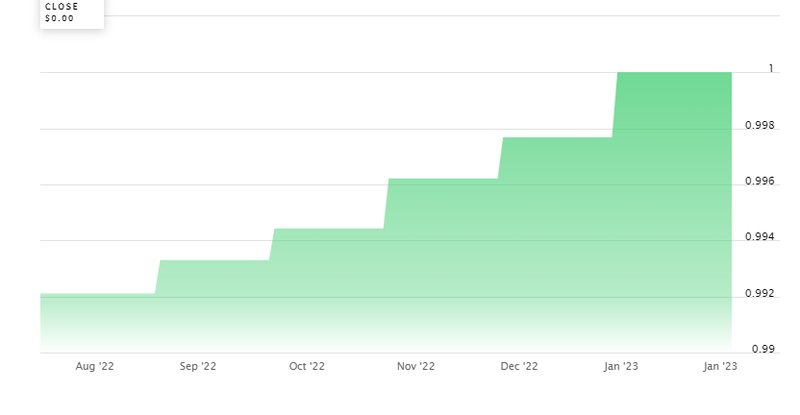

Fine wine returns aren’t affected by market factors such as an interest rate hikes and inflation. In fact, the finest wines usually deliver stable returns that aren’t correlated to conventional investment assets like stocks.

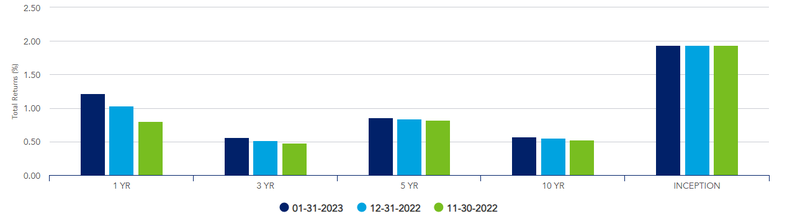

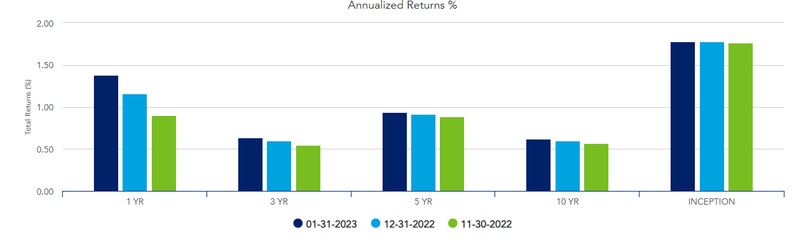

For example, fine wine returns were around 26% during the Great Recession in 2008, while traditional stocks fell by 52%.

In addition, fine wine returned more than 11% in 2022. Its two-year returns were 36.8%, while the five-year returns reached 50.3%.

So, how do you invest in fine wine?

Visit the Vinovest website — a reliable investment platform that lets you buy, store, and sell investment-grade wine bottles.

Here are the steps you need to follow:

- Sign up on the Vinovest website.

- Answer a quick questionnaire to determine your risk tolerance and investment style.

- Fund your account with a minimum payment of $1,000.

- Sit back and watch your investment portfolio grow.

Here are some of the benefits of investing through Vinovest:

- Vinovest stores your bottles in bonded warehouses and doesn't charge you any excise duty or VAT.

- You can access investment-grade wines without the ridiculous retail markup or intermediaries.

- Vinovest procures all the wine directly from wineries, merchants, and wine exchanges. This strategy ensures you buy your wines at the best possible wholesale prices.

- Vinovest makes wine purchasing accessible. There's no need for expertise, as the platform has a team of knowledgeable sommeliers.

- Vinovest’s Artificial Intelligence (AI) platform lets you buy and sell wine from anywhere in the world.

- Vinovest authenticates every single bottle and checks its provenance before you buy them. This ensures that you avoid purchasing counterfeit bottles.

- Vinovest has a comprehensive insurance policy that’ll give you peace of mind knowing that your wines are safe and well-maintained.

Diversify Your Portfolio By Investing in Fine Wine and Money Market Funds

Money Market Funds are a good option for anyone who’s looking for short-term investments. But these assets tend to be volatile and usually underperform during economic downturns like inflation.

Want a profitable asset that offers stable returns despite market swings?

Invest in fine wine today! Visit the Vinovest website and start investing in the best wine bottles from around the globe.