Wine and Equity Have More in Common Than You Might. Just Ask the Fed

Further reading

- Have a sweet tooth? Here’s your perfect guide to Sweet Wines.

- You may also want to check out the 5 Reasons You Should Invest In Wine!

Monetary policy is an important tool to manage the intricate balance between price stability and maximum sustainable employment - a dual mandate that the Federal Reserve received from Congress.

As the Fed increases interest rates under Jay Powell, banks are incentivized to hold money in reserve rather than lend it. As a result, we’ve seen a cooling down of the loan supply and, therefore, economic activity. With inflation rates the highest they’ve been since 1982, the Fed has to act and enforce a stricter monetary policy to defend its credibility like in the Volcker era.

On the other hand, when the Great Recession hit in 2008, the Federal Reserve lowered interest rates to near-zero. Using other financial instruments, the Fed has sought to maintain a high money velocity and encourage economic activity and employment.

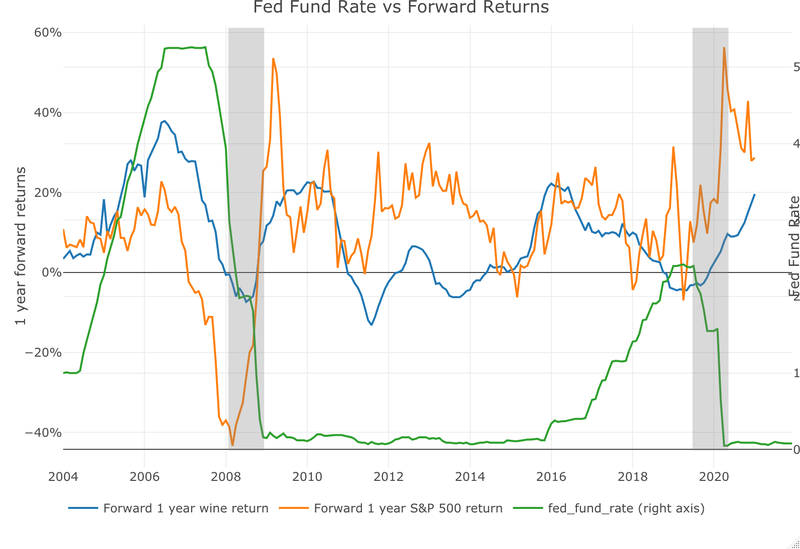

Naturally, these monetary policies have a wide-ranging impact. I wanted to run a simple exercise to see how the Fed’s decisions affected wine prices and equity prices as a benchmark. The goal is to see how wine prices respond to the Fed Funds Rate (FFR) change.

The wine prices used in this exercise were tracked using the Liv-Ex 1000 Index, which has data dating back to 2004. Below is a chart illustrating the 1-year forward returns for the Liv-Ex 1000 Index and S&P 500. On the right axis, I measured the FFR.

Over the last 17 years, there were two major periods with prolonged FFR increases. Those areas (2004 to 2006 and 2016 to 2018) are highlighted in gray. Before 2004, the economy suffered a mild recession in 2000-2001 and a tech bubble, but FFR increases were done in a strong economy that continuously performed well.

The Fed pivoted in the mid-2010s with its use of quantitative easing (QE). The Fed bought assets outright from the market, increasing the money supply and sustaining asset prices. This monetary policy came when the market was more nervous, and the pace of price increases was going down for both equities and wine.

In 2007 and the second half of 2019, the FFR plateaued. The market was looking ahead in anticipation of recession and deflation. Both times, the equity markets responded negatively. Wine was slower to react in the second half of 2019 due to the short time frame.

It wasn’t until 2020 that the Fed slashed the FFR, doing so more than the market expected. The decisive action reinvigorated risk-taking, and asset prices skyrocketed. That happened in conjunction with the Great Recession and the Covid-19 Recession. Both wines and equities were not an exception.

Conclusion

Equities and wines, as with any other risk assets, are responsive to FFR. Wine is less sensitive to the FFR and changes happen more smoothly than equities, both up and down.

You might say, what about the future prices here? The data shows mixed signals here. In one environment (2004 to 2006), the price acceleration increased. In another environment (2016 to 2018), it did not. The future prices depend on the demand for each asset class during the FFR increase or the anticipation of it.

Long story short: Do not fight the Fed! The monetary policy has a big effect on the assets and as investors you should closely watch their actions.

Note that the Fed Funds Rate is predictive of the second order of price (price acceleration or deceleration, but not the price changes). The level of change of FFR is not showing a relationship with future price changes.