Vinovest Quarterly Report Q3 2025

The third quarter of 2025 marked a tentative turning point in the fine wine and whiskey markets. After nearly two years of headwinds, we observed early signs of stabilization: fine wine indices firmed up, whiskey investors adjusted to a new normal, and macroeconomic shifts began to favor alternative assets. Here’s how wine, whiskey, and the broader landscape fared in Q3 2025.

Further reading

Catch up on last quarter's report here.

By The Numbers

- 0.4% – Q3 2025 gain for the Liv-ex Fine Wine 100 index, marking its first quarterly increase since the market downturn began.

- –0.5% – Q3 2025 change for the Liv-ex Fine Wine 1000 index, a broad benchmark of 1,000 investment-grade wines, reflecting a modest dip as prices neared a bottom.

- 3.9% – Rise in global whiskey export volumes in 2024–25, even as total export value fell ~3%, indicating resilient demand for spirits at lower price points.

- 97 – Points (from both Vinous and Wine Advocate) awarded to Taittinger Comtes de Champagne 2014, drawing comparisons to the legendary 2008 vintage and underscoring Champagne’s continued appeal.

Fine Whiskey Performance in Q3

The global whiskey market in Q3 2025 experienced a tale of two tiers. On one side, whiskey exports remained robust in volume but underwhelming in value: for example, Scotch whisky shipments reached 1.4 billion 70cl bottles in 2024 (about 44 bottles per second), up nearly 4% by volume despite export values dipping ~4%. This trend of consumers gravitating toward more affordable pours left premium and super-premium segments struggling. Japanese whisky exports similarly softened, dragged down by weaker demand in key markets like the US and. In the US, American whiskey producers faced a growing glut – domestic sales stagnated while inventories hit record highs (nearly 1.5 billion proof gallons aging in barrels, triple the 2012 volume). With U.S. distillers counting on exports to relieve this oversupply, a mid-year slump in overseas sales was unwelcome news: American spirits exports fell 9% in Q2 (year-on-year), including an 85% plunge to Canada amid trade frictions. Tariff aftershocks and foreign consumer boycotts have clearly made their mark, putting U.S. whiskey makers under “mounting pressure and financial strain” according to the Distilled Spirits Council.

Meanwhile, the secondary market for rare whiskey showed signs of finding its footing after two years of correction. According to Noble & Co’s Whisky Intelligence Q3 2025 report, the spring/summer period saw the whisky auction market “settle into a new rhythm” following a ~40% decline in trade value from late 2022 peaks. The frenzy of flippers flipping and speculative buyers has largely receded, leaving a core of patient investors and collectors who are now driving a cautious recovery. Importantly, a new balance between supply and demand is emerging at lower price points. High-end trophy bottles that once commanded astronomical prices have seen prices soften from their apex – for instance, even famed Macallan releases are trading below last year’s highs.

Yet demand for cult and mid-tier whiskies remains steady. In-demand releases from beloved distilleries like Ardbeg and Springbank continue to move briskly in the £100–£500 range, providing liquidity and stabilizing the market. Q3 saw its share of headline-grabbing auction sales (a Bowmore “Arc-54” Iridos edition fetched £112,500 in one sale) – proof that appetite for rare bottles hasn’t vanished. However, buyers are exhibiting greater price discipline and selectivity than in the boom years, seeking provenance and value over hype.

Regulatory tailwinds are also shaping the whiskey landscape. The official recognition of American Single Malt Whiskey as a category (a late-2024 development) began to bear fruit in 2025. With U.S. standards in place, large producers and craft distillers alike spent Q3 ramping up releases in this nascent category, aiming to tap consumer curiosity. This comes as the American whiskey industry eyes any edge to chip away at sky-high inventories. In Scotland, no similarly dramatic regulatory shifts occurred in Q3, but the industry kept a close watch on trade policies. A stronger British pound earlier in the year and lingering tariff uncertainties have kept exporters vigilant.

Overall, premium whisky is entering an era of more measured growth. The Q3 data suggests that after a period of overshooting and correction, the whiskey market is finding equilibrium. Super-premium Scotch and bourbon may not be racing back to their 2021 price peaks, but the long-term fundamentals – a 20-year, 2000%+ boom in high-end whiskey revenues through 2023 – remain intact. As our whiskey experts put it, this is an “exciting opportunity” for diversification into whiskey while the market is momentarily subdued. For investors, the takeaway from Q3 is to mind the gap between tiers: value-driven bottlings and new categories are showing resilience, whereas ultra-rare trophies might require a longer hold until the next upswing

Fine Wine Performance in Q3

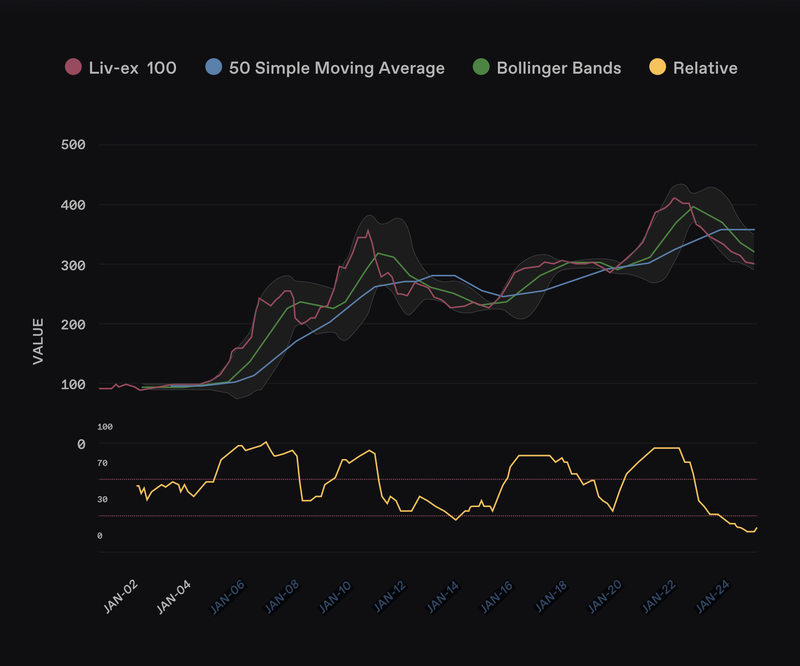

After eight consecutive quarters of price drift, the fine wine market in Q3 2025 finally showed signs of stabilizing – and even a glimmer of growth. The Liv-ex fine wine indices, which track real-time transaction prices, suggest that the worst of the correction may be behind us. The elite Liv-ex 100 index (the “Fine Wine 100”) notched a +0.4% gain for the quarter, its first quarterly uptick since early 2022. This modest rise was powered by a strong September: the index jumped 1.1% that month amid a surge in buyer interest and improved bid/offer dynamics. By September’s end, the Liv-ex 100’s bid-to-offer ratio – an indicator of market sentiment – had climbed to 0.70, its highest level since April 2023. In other words, for each £1 of wine offered for sale, 70p was wanted by buyers, signaling a healthier balance than the sub-0.5 ratios seen throughout 2024. The broader Liv-ex Fine Wine 1000 (the industry’s 1000-wine composite index) was still down 0.5% over Q3, but even that index mirrored the late-quarter recovery rally. For context, 18 of the last 19 months prior had been negative for the 1000 index, so a near-flat quarter feels like a victory for wine investors. Market activity also perked up: September’s trading on Liv-ex saw trade value up 9.5% and volume up 6.4% compared to the Q3 average, approaching liquidity levels not seen since the pre-tariff era of 2019.

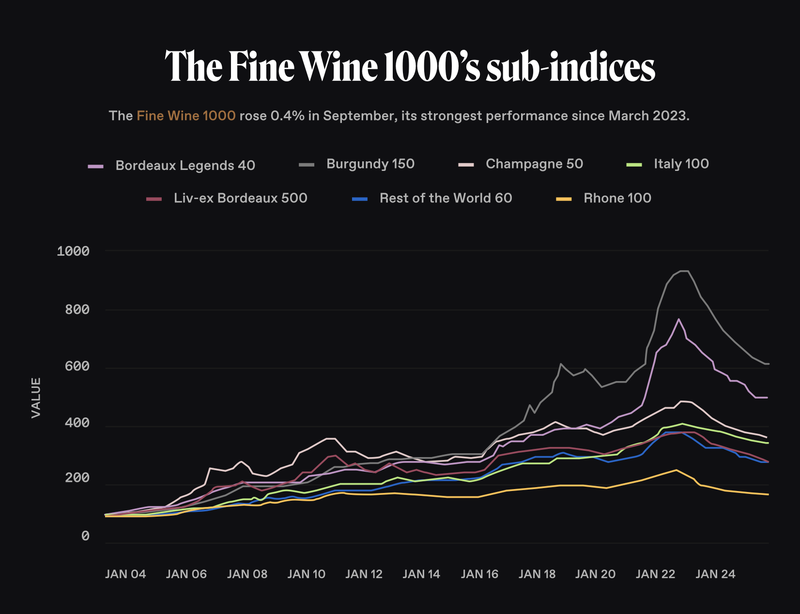

Beneath the headline numbers, Q3’s performance varied by region and price tier. Champagne remained a stalwart – the Champagne 50 sub-index held flat (0.0%) for the quarter, effectively making it one of the best-performing regions in a generally soft market. Steady U.S. and Asian demand for top Champagne houses kept prices buoyant. Rhone wines also inched into positive territory, reflecting how value-driven regions are attracting renewed interest. Notably, the Italy 100 index rose about +0.4% in Q3, and the Rest of the World (RoW) 60 – which features New World cult wines from Napa, Australia, etc. – ticked up +0.3%. On the flip side, the heavyweights are still finding their footing: Bordeaux fell –1.7% over the quarter, and Burgundy dipped –0.2%. These declines, however, were far milder than the drops of 2022–2024, and by September even these regions hinted at a bottom. Liv-ex reported that several key Bordeaux sub-indices (including the First Growths and Right Bank 100) turned positive in the final month of Q3. Indeed, September saw Bordeaux’s “Legends 40” index – an index of esteemed mature Bordeaux vintages – jump +1.8%, making it the month’s best-performing sub-index on Liv-ex. Likewise, the Burgundy 150 index bounced +0.8% in September, although many Burgundy blue-chips are still only at their 2020 price levels. Even the long-unloved Bordeaux First Growths showed life: the Liv-ex Fine Wine 50 (tracking recent vintages of Lafite, Mouton, Margaux, etc.) saw its first rise in three years. All told, while Q3 wasn’t a broad rally for every wine, it decisively broke the pattern of steady decline and may have established a floor for the most beaten-down segments.

Digging deeper, trading patterns and notable price shifts in Q3 reaffirm that selectivity is key. The gap between the market’s winners and losers widened, underscoring an increasingly selective recovery. The best-performing wines of 2025 (year-to-date) are up an average of +18%, even as the Liv-ex 1000 index remains ~–4.7% YTD. What’s driving these winners? Scarcity and quality. Some previously overlooked “off-vintage” gems came into favor as bargain hunters recognized their value. For instance, once-maligned Bordeaux vintages 2013 and 2014 suddenly saw interest for their approachability – Château Les Carmes Haut-Brion 2013 surged +38.2%, while Château Beychevelle 2014 climbed +22.2% this year. Rhone wines quietly delivered steady gains as well, proving that top-notch Châteauneuf-du-Pape and Hermitage bottlings (e.g. Vieux Télégraphe 2020, Jaboulet La Chapelle 2014) can shine even in a sluggish broader market. And at the very high end, true blue-chip icons never really went out of style – Domaine de la Romanée-Conti, Screaming Eagle and their ilk continued to attract strong bids in Q3, reaffirming that rarity + prestige = enduring demand. Among regions, Champagne’s resilience deserves special mention. A star of the past few years, Champagne held value in Q3 and even produced a new star of its own: Taittinger’s Comtes de Champagne 2014. This tête de cuvée earned 97-point scores from multiple critics and is being talked about as the next legendary vintage after 2008 – a comparison that is driving up its collectability (the 2008 now trades at ~40% above release price). The 2014 Comtes’ combination of critical acclaim, relative affordability, and scarce production encapsulates why Champagne remains a cornerstone of many wine portfolios. In short, Q3’s fine wine market was defined by selective strength: broadly flat overall, but with pockets of exuberance for the right wines.

Investing Outlook for Q4 and Beyond

As we head into Q4 2025 and beyond, the outlook for fine wine and whiskey is cautiously optimistic – data-driven, yet tinged with the hard-earned lessons of the past two years. The overarching theme from our experts is one of guarded optimism: markets appear to be stabilizing, but nobody is calling for an immediate return to roaring bull days. Instead, we anticipate a slow grind upward, underpinned by selective opportunities and a healthier balance between buyers and sellers.

For fine wine, all signs point to the market finding its equilibrium. The recent improvement in the bid:offer ratio on Liv-ex (now around 0.6–0.7 after languishing below 0.5 in 2024) suggests that buying interest is gradually returning relative to supply. If this trend holds, prices should follow. In other words, the expectation is for organic growth rather than speculative spikes – a welcome scenario for long-term investors. Several macro factors will shape the fine wine landscape in late 2025 and 2026. Currency movements are key: the strength of the U.S. dollar versus the British pound has already influenced regional demand (a strong GBP made European wines pricier for USD-based buyers in 2024, whereas any firming of the USD going forward could boost American buying power again). Trade policy is another wild card. Tariffs remain a looming specter – the U.S. administration’s flirtation with new import tariffs on European wines (after the suspension of the 25% tariffs in 2021) has the industry on alert. Any imposition of duties could temper U.S. demand overnight, a concerning thought given Americans accounted for over one-third of Liv-ex trade by value in 2024. In Europe, the backdrop includes sluggish economies and even some tax changes (the UK, for instance, raised alcohol duties in 2023). Indeed, global wine producers face a paradox entering 2026: historic supply shortages but tepid demand. The 2025 northern hemisphere harvest is forecast to be one of the smallest in decades – potentially the lowest global wine output since 1961 – owing to harsh weather and vineyard reductions. Normally, such a supply crunch might trigger price spikes, but so far we’re seeing the opposite: weak end-consumer demand and high retailer inventories are preventing any surge. As the New Zealand Winegrowers’ report noted, short crops “no longer drive demand” like they used to. This dynamic should keep fine wine prices relatively stable and range-bound in the near term, a silver lining for buyers who can selectively acquire quality assets at 10–20% discounts from their peaks. We also see opportunities emerging in this environment: off-vintage Bordeaux and under-loved regions (Rhone, Spain) offer bargains that could rally when the market fully recovers. And of course, Champagne and Italy remain defensive plays – their steady performance through the downturn suggests they’ll be early leaders in a rebound.

For whiskey, the investment outlook is one of measured recalibration. The past two years have humbled the exuberant growth trajectory of rare whiskey, but in doing so, they’ve likely set the stage for a more sustainable climb ahead. Our whiskey experts point to the recent stabilization as a sign that the market’s base is solidifying. With speculative “flip” buyers largely gone, the field is clearer for true collectors and long-horizon investors. American whiskey, in particular, faces an inflection point: producers must work through their record inventories, which could mean some attractive pricing or cask investment opportunities for buyers with patience. However, resolution of trade disputes will be critical – continued export barriers (or consumer boycotts) could force distillers into domestic oversupply and keep a lid on short-term returns. We’ll be watching negotiations with the EU and other partners closely; any positive trade developments (or extension of tariff suspensions) would lift a big weight off American whiskey’s shoulders. On the Scotch side, the market is expected to remain bifurcated: the ultra-rare segment may lag as it rebuilds from its correction, whereas the middle market – think independent bottlings, limited editions from cult distilleries, and newly recognized categories like American Single Malt – could offer outsized returns. In the words of Vinovest’s spirits specialists, this is a time to “look at everything from an individual perspective” rather than assuming broad category-wide gains. A focus on high-quality casks with real scarcity, strong provenance, and passionate followings will be key. Encouragingly, the whisky secondary market’s first hints of stabilization in 2025 indicate that a floor has been found. Noble & Co’s report suggests the worst of the price swings are over, with volumes picking up and buyers returning, albeit at more reasonable price points. Going into Q4, we expect to see sideways or gently rising prices for most collectible whiskey, rather than further steep declines. There is also optimism that macro trends (e.g. potential interest rate cuts in major economies and robust equity markets) will spill over into renewed appetite for alternative assets, whiskey included.

In summary, Q4 2025 and beyond look to be a period of consolidation and selective growth for wine and whiskey. Investors should take comfort that these markets have weathered the storm and are now arguably healthier – characterized by more realistic pricing, motivated buyers, and sellers willing to deal. It’s a far cry from the exuberance of 2021, but that’s not a bad thing. “When you’re in it for 10 to 15 years, you don’t really want boom and bust…really what we hope for is a sustainable global market,” as our Head of Trading wisely reminds us. The playbook for the coming months is clear: diversify, focus on quality, and be patient. Whether it’s acquiring a top Burgundy at a 30% discount from its highs, or tucking away a few barrels of bourbon now classified as “straight” whiskey, the opportunities are increasingly favoring the disciplined, long-term investor. Both wine and whiskey markets are poised to enter 2026 on a steadier footing – and those who have stayed the course may well toast the loudest when the next upswing finally arrives.