Vinovest Quarterly Report Q4 2025

The final quarter of 2025 represented a significant technical milestone for both the fine wine and spirits markets: the establishment of a definitive price floor. After nearly three years of consistent downward pressure, the major wine indices recorded three consecutive months of gains starting in September, concluding the year with renewed stability. While total wine trade value for 2025 was down 5.8% compared to the previous year, trade volumes increased by 7.2%, signaling that the "stock clear-out" phase is maturing into active collector re-entry. Similarly, the whiskey market entered a "Great Correction" where the softening of speculative mid-market retail prices was met by a historic auction boom. Collectors are increasingly benefiting from a "flight to quality," where meticulously aged expressions are becoming accessible at rational price points even as "unicorn" bottles continue to shatter records. Across both assets, the entry of younger, international capital – particularly from Europe and Asia – is providing a robust new foundation for the market.

Further reading

Catch up on last quarter's report here.

By The Numbers

- +0.4%: The rise in the Liv-ex Fine Wine 100 index in December, marking a shift toward year-end stability.

- 1.6%: The gain recorded by the Rhône 100 in December, the only sub-index to finish 2025 with positive returns.

- 37.9%: The percentage of Fine Wine 1000 components that saw a price decrease in December – the lowest proportion in over three years.

- $162,500: The record-shattering auction price for a bottle of Old Rip Van Winkle 20-Year-Old, a new benchmark for American whiskey.

- 12,000+: The record number of unique vintage-and-label combinations traded in 2025, highlighting unprecedented market breadth.

- 50%: The percentage of whiskey auction buyers in 2025 who were under the age of 50, signaling a major demographic shift in global collecting.

Fine Wine Performance in Q4

Last quarter of 2025 was defined by a contraction in volatility rather than a vertical price surge. In December, only 37.9% of the Fine Wine 1000 components saw price decreases – the lowest proportion of fallers since September 2022.

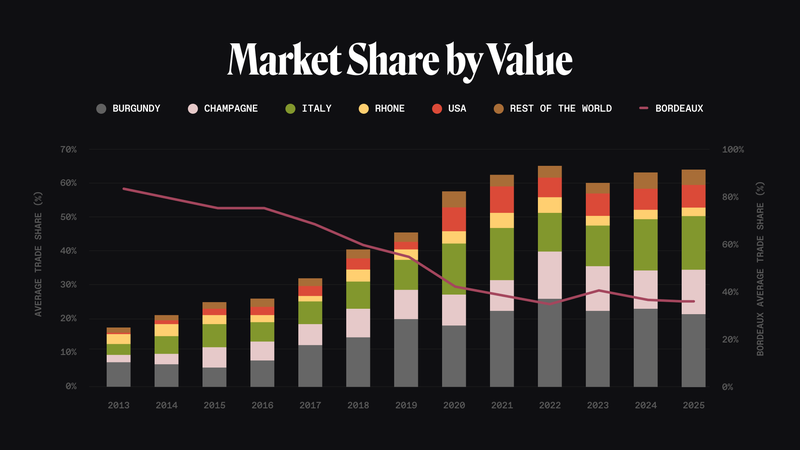

- Breadth of Trade: The market reached a record level of diversification in 2025, with over 5,000 unique labels and 12,000 unique vintage-label combinations traded.

- Activity Levels: Despite price stability, Q4 2025 trade volume and value remained lower than Q4 2024 levels, down 7.2% and 9.2% respectively, as the market adjusted to new global trade dynamics.

Regional Performance: Standouts and Laggards

Rhône: The Resilience Leader

The Rhône 100 was the star performer of 2025, leading the sub-indices with a 1.6% gain in December and finishing the year as the only major index to post positive returns.

Bordeaux: Stability at the Top

After a period of prolonged adjustment, Bordeaux indices like the Fine Wine 50 (+0.7% in Dec) have begun to flatten out. While the Bordeaux 500 saw a marginal 0.1% dip in December, the broader trend is one of consolidation, particularly for top-tier estates.

Underperformers: The Second Wine Slump

The most significant corrections in 2025 were concentrated in Bordeaux’s second wines and the Right Bank. The Second Wine 50 (-9.4%), Right Bank 100 (-8.2%), and Right Bank 50 (-7.3%) faced the steepest declines as buyers shifted focus toward primary labels.

The Global Shift: Europe Steps Up

The introduction of 15% tariffs on European wine in April 2025 fundamentally altered trade flows.

- US Retreat: Previously the market’s most significant buying segment, US activity was muted throughout H2 2025 as the trade grappled with increased costs.

- European Dominance: European buyers aggressively filled the void, with total purchase value from the region surging 48.2% year-on-year.

- Asian Recovery: Signs of "green shoots" in the Asian market began to emerge in Q4, providing a crucial secondary pillar for global price support.

Q4 2025 Whiskey Investment Performance: A Divergent Landscape

The final quarter of 2025 crystallized a defining theme for the whiskey market: a "Great Correction" in secondary market retail prices juxtaposed against a historic "Auction Boom." While broader indices such as the Whiskystats Whiskey Index saw values soften as the market recalibrated from the speculative highs of 2021–2023, the ultra-rare segment demonstrated staggering resilience. Collectors are currently benefiting from a "flight to quality," where meticulously aged expressions are becoming accessible at more rational price points, even as "unicorn" bottles continue to shatter records at major auction houses.

Market Overview: Price Softening vs. Depth of Demand

Q4 2025 marked a departure from the tentative stabilization seen in Q3. Secondary market trading values continued to consolidate, particularly in the mid-range investment tier.

- The Valuation Gap: According to Whiskystats, the setback in trading value in Q4 outweighed a downturn in volume. This indicates a "buyer's market" where sellers are adjusting expectations to meet a more disciplined collector base.

- Demographic Shifts: Auction data from Sotheby’s reveals that nearly 50% of buyers in 2025 were under the age of 50, and 33% were new to the market. This influx of younger, international capital from Asia and the Middle East provides a robust long-term support level for the asset class.

Regional Performance: Bourbon Ascendant, Scotch Consolidates

American Whiskey: Breaking the Ceiling

Q4 2025 was a watershed moment for Bourbon. For the first time, Van Winkle entered the top three spirits brands by value at Sotheby’s.

- Record Breaking: A bottle of 20-year-old Old Rip Van Winkle fetched $162,500 in 2025, a new benchmark for American whiskey.

- Supply Dynamics: While production in the US has contracted by 20% year-over-year, the scarcity of ultra-aged (8+ year) barrels remains acute, supporting premiumization in the secondary market.

Scotch Whisky: The Macallan Standard

The Scotch market remains the cornerstone of global trade, with The Macallan maintaining an 18% share of all spirits auction value at major houses.

- Mature Malts: Long-aged whiskies (40-60+ years) from legacy distilleries like Bowmore, Dalmore, and Brora remained the primary volume drivers for high-value lots.

- Index Performance: The Rare Whisky 101 Apex 1000 has reflected the broader luxury correction noted by Knight Frank, showing a cumulative decline from the 2022 peak but finding support as European and Asian buyers increase their market share to 37% and 31% respectively.

Japanese Whisky: Stability in the Ghost Tier

While some mid-market Japanese labels have seen prices "nose-dive" according to annual auction summaries, the "Ghost Distillery" tier remains untouchable. The record-setting £4.25M sale of two Karuizawa casks at Christie’s in late 2025 underscores that unique, unrepeatable assets are decoupled from broader market softening.

Investing Outlook for 2026

Heading into 2026, the market is expected to "bump along the bottom," offering a unique opportunity for disciplined accumulation before the next growth cycle.

- Wine Catalysts: The primary "gear-shifts" for the coming year will be the pricing of the promising 2025 Bordeaux En Primeur campaign and the outcome of lobbying efforts against US tariffs. If these efforts successfully unlock US demand to join the increased European and Asian activity, the market could decisively turn the corner. .

- Whiskey Divergence: We expect the spirits market to remain bifurcated. While broader indices may remain soft as they recalibrate from 2021–2023 highs, the ultra-rare segment – led by legacy Scotch distilleries and the institutionalization of American Bourbon – is poised for continued resilience.

Collector Opportunity: This extended period of horizontal movement gives new collectors the chance to build sustainable portfolios based on quality and utility rather than speculation. For those prioritizing long-term value, the focus remains on blue-chip assets that have found stability and are now narrowing the gap between trade and market prices.