10 Foolproof Retirement Investment Strategies To Try Now

No matter your age, planning for retirement living is super-important.

But what retirement investment strategies should you adopt?

You probably want to maintain your current lifestyle (if not something 10x better!) when you’re ready to retire. Right?

The good news?

This process doesn’t have to be overwhelming — especially with our top 10 retirement investment strategies and essential planning tips to remember.

We’ll also tell you about one of the best time-tested long term investments - fine wine.

Further reading

- How do you protect your investments from market fluctuations? Discover the 8 Sectors That Benefit From Inflation.

- Find out All About the Retirement Bucket Strategy and set yourself up for a care-free retirement

10 Proven Retirement Investment Strategies

Here are some investment strategies to consider when planning your retirement:

1. Invest in Long-Term Options Right Away

One of the best retirement investment strategies includes setting up attractive long-term investments.

Why?

Long-term investments generally help you ride out the market drops, and give you the powerful benefit of compound returns.

And, some of them offer excellent returns too.

Our top picks are:

A. Fine wine

Investing in fine wine is no longer only for the rich and famous. It’s easily accessible to anyone – whether you’re planning a retirement nest egg or not.

Wine investing is an excellent investment strategy for a few reasons:

- Inflation-proof: When inflation rises, fine wine prices also increase. It usually delivers positive returns and outperforms the CPI (Consumer Price Index.) While the US average annual inflation rate in 2021 was 5%, the wine market grew by around 23%.

- Excellent returns: Fine wine has enjoyed a compound annual growth rate of 11% since 1988. Plus, fine wine performs better than traditional stocks. For example, the Liv-ex 100 index earned returns of 22% between 2021 and 2022, while the S&P 500 index produced -5% returns.

- Price appreciation: The longer fine wine ages, the rarer it becomes, thus appreciating in value.

The best way to invest in fine wine?

Vinovest is a wine investment company that helps you buy, store, and sell fine wineanywhere in the world.

It offers many exclusive benefits, including:

- Easy buying and selling: You can buy and sell at any time. Fine wine hits its peak after 5-20 years. So Vinovest’s advisors will help you identify the best liquidity options and time periods to sell, ensuring you maximize your return on investment.

- Super prices: Vinovest sources bottles directly from wineries, merchants, and wine exchanges at wholesale prices.

- Optimal storage: Vinovest stores your wines in bonded warehouses under excellent light, humidity, and temperature conditions.

It’s super easy to sign up. All you have to do is:

- Sign up on the Vinovest website with your personal information.

- Answer a questionnaire to determine your risk appetite and investing style.

- Add a minimum of $1,000 to your account.

- Sit back and watch your account grow!

B. Real Estate Investment Trusts (REITs)

Investing in a REIT is a great retirement option. You can easily invest in real estate properties without ever having to buy property.

So what’s a REIT?

A company classed as a REIT owns, operates, and finances real estate properties to obtain rental income.

When you invest in this asset class, you can earn quarterly or annual dividends.

This makes a REIT a fruitful fixed income stream and an excellent inclusion in your investment strategy.

What’s more?

You don’t have to actually manage or maintain these properties.

That’s not all — you can choose from various REITs to suit your interests and needs. Many REITs span different industries (think retail, healthcare, offices, and residential.)

C. Dividend Fund

A dividend fund is a type of mutual fund that invests only in equity shares (partial ownership of a company.)

These equity shares pay regular dividends.

A dividend fund may be for you if you want consistent income. Just remember that your earnings will depend on how the market performs.

D. Large-cap Stocks

Large-cap stocks (or big-cap stocks) are released by massive companies with a market capitalization of $10 billion or more (think Microsoft, Amazon, and Apple.)

It’s a good long-term option if you’re looking for high dividend payouts (expect on average about 10.2% annually), stability, and good management.

2. Regularly add to your 401K Plan

A 401K plan is a tax-advantaged account that your employer sponsors. All money go towards your retirement.

But how does it work?

It’s simple.You just invest a portion of your paycheck directly into your 401K account. In turn, your employer may match a part or all of your contributions.

But remember: When you withdraw these funds at retirement, expect income tax fees. You don’t get taxed for contributing to your 401K plan, but you will be at the time of withdrawal.

Another thing to keep in mind:If you tap into these funds before you hit retirement age, you can get heavily taxed. This includes a 10% penalty fee when you retire and a 20% withholding tax

Alternatively, you can open a Roth 401K where you contribute after-tax funds. With a Roth 401K account, you can withdraw your funds tax-free after retirement.

3. Open a Health Savings Account

Let’s face it:The older you get, the more your healthcare bills increase.

Prepare for this early on by setting up a Health Savings Account. It’s a personal savings account where you make regular contributions to pay for certain medical costs like medication, doctor visits, and dental and vision care.

You can grow and withdraw this money tax-free if you use it for qualified healthcare expenses.

4. Create a Retirement Income Fund

A retirement income fund (RIF) is a mutual fund with a good diversification of large and mid-cap stocks and bonds.

Such funds are treated as regular mutual fund investments and make regular payments every month or quarter.

Remember:

- Use this fund to supplement other sources of retirement income.

- Watch out for retirement fund fees.

- Research to figure out what the lowest fees are before diving in.

5. Start an IRA, Roth IRA, SIMPLE IRA or SEP IRA

Let’s explore these retirement account types:

- IRA: A traditional IRA (individual retirement account) allows you to make tax-deductible contributions and tax-free growth. Your earnings don’t get taxed until you make a withdrawal. You set up a traditional IRA through a private financial institution (think bank or brokerage.)

- Roth IRA: This type of account is a unique tax-advantaged IRA that allows you to contribute after-tax dollars. Once you’ve made your contributions, it grows tax-free. And if you’ve had your Roth IRA account for over five years, you will not face taxes or penalties.

- SIMPLE IRA: A SIMPLE (Savings Incentive Match Plan for Employees) IRA is made especially for small businesses with 100 or fewer employees.

You make regular contributions, and your employer will make either matching or nonelective contributions.

- SEP IRA: A SEP or Simplified Employee Pension Plan allows only employers to contribute towards their employees' retirement. Your employer can contribute up to 25% of your annual pay up to $61,000. You can contribute to your own SEP IRA.

Your money is only taxed when you make a withdrawal. And you incur a penalty fee if the money is uplifted before you turn 60.

6. Hold on to Social Security Benefit Collection

Did you know that the longer your wait to collect your earnings, the more you get?

Under the social security plan, the full retirement age is 66 years old. So if you hold out on collecting until after the full retirement age, you can increase your annual payments easily.

What’s more?

If you’re between full retirement age and 70 and have already started collecting funds, you can still capitalize on earnings. Just request payments to be suspended to maximize your future profits.

7. Identify Your Risk Tolerance

If you’re nearing retirement, you may be less risk tolerant when building a portfolio.

Some of your investments may provide excellent returns but can also have high risk levels.

There are many types of investment risk, including:

- Market risk: As an investor, you experience losses due to financial market instabilities.

- Interest rate risk: When interest rates fall, bond prices (and other fixed rate investments) rise and vice versa.

- Inflation risk:Inflation can weaken an asset’s value, investment, or purchasing power of an income stream.

- Credit risk: This is the measure of the creditworthiness of a borrower.

So count in all the relevant risk factors to figure out your risk tolerance and risk management strategies.

8. Get An Annuity

Outliving your retirement saving nest egg can be a scary thought. You can protect yourself through annuities.

An annuity is an insurance contract issued by financial establishments where you make a lump sum or a series of payments.

This money is then paid as regular fixed income immediately or at a predetermined future point during retirement.

Here are a few types of annuities available:

- Fixed annuity: A fixed annuity pays a set amount every month for a certain amount of time. You receive this income during a pre-determined time frame.

- Immediate annuity: For a lump sum payment, you will receive a set income for a predetermined time frame.

- Variable annuity: This type of annuity is tied to the performance of an investment portfolio of sub-accounts and mutual funds. So how much you receive will depend on how the portfolio performs.

9. Factor in Inflation

So far, so good. You’re regularly setting money aside for retirement, and your retirement funds are steadily growing.

But have you factored in inflation?

As of August 2022, inflation has risen to 8.26%. So whatever money you’re setting aside for retirement, calculate inflation on top of it.

This way, you won’t have to worry too much about your money losing value by the time you’re ready to retire.

10. Put Down a Withdrawal Strategy

So you’ve figured out where you want to invest your money based on your individual situation.

But how much and how often will you withdraw from your retirement accounts?

The pros recommend creating a withdrawal strategy (like systematic withdrawals) at least five years before retirement.

If you’re unsure how to go about this, discuss it with your financial advisor.

Remember to watch out for additional fees, taxes, and penalty charges for early withdrawals.

Let’s now explore a few tips to guide you through planning for retirement.

8 Tips to Remember While Creating Your Retirement Plan

There’s no one size fits all retirement plan — it has to evolve with your career and goals.

Remember these eight tips while making your retirement plan — trust us, it’ll give you an extra measure of security:

- Establish When You Want To Retire and Make a Strategy Based on That

- Figure out Realistic Spending Habits

- Keep An Eye On Taxes

- Start Saving 15% (or More) a Year

- Rebalance Asset Allocation

- Create an Estate Plan

- Analyze Your Investments

- Get Retirement Planning Assistance From A Financial Professional

1. Establish When You Want To Retire and Make a Strategy Based on That

Figure out when you want to retire and then work backward.

Doing this will help you determine how much time you have to get your finances in order.

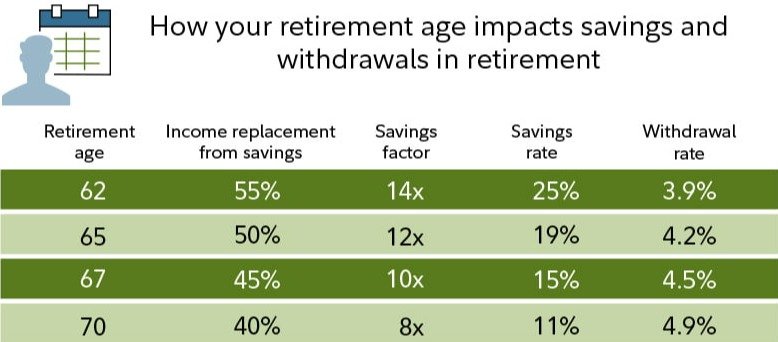

Depending on your age, here are a few retirement strategy suggestions:

20-30s age group:

- Have a mix of 70-75% stocks, 15-20% bonds, and 10-15% cash.

- Be aggressive and focus on compound interest and pay off loans.

- Have a 3-6 month emergency fund for healthcare bills or job loss.

40-50s age group:

- Have an investment mix of 30-50% of stocks, 60-40% bonds, and 10% cash.

- Reallocate some funds into fixed income investments.

- Pay off any mortgage and consider downsizing your home.

- Take advantage of employer-sponsored retirement accounts.

60s age group:

- Have a mix of 20% stocks, 70% bonds, and 10% cash.

- Move the bulk of your savings into fixed income bonds and plan your withdrawal strategy.

- Map out your legacy plan and sort out your estate documents and will.

2. Figure out Realistic Spending Habits

Identify how much income you want to have post-retirement. Take into consideration realistic expenses, including medical and travel costs.

Your most significant financial expenses will likely include:

- Housing: Free up hundreds of dollars by buying or renting a space enough for you. And aim for affordable housing locations.

- Food: According to the Department of Agriculture, Americans waste about 30% of food. Assuming the average household sets aside 13% of its budget for food, that’s about 4% of your annual earnings getting thrown out. To avoid that, be mindful when buying groceries - try to buy just enough, so nothing gets thrown out.

- Transport: Buying a new vehicle is an expensive affair. So, focus on a small or midsized fuel-efficient car that you can enjoy for at least 15 years.

3. Keep An Eye On Taxes

Here’s the deal:

When building your retirement portfolio, don’t forget about possible tax implications.

Most investment options (like IRAs) let you choose if you want to be taxed now or at withdrawal time.

Spend time figuring out how certain investment gains are taxed so your future returns will not be impacted.

4. Start Saving 15% (or More) a Year

The pros recommend investing 15% of your household income annually.

If you start doing this by 30, you can retire by about your mid-60s.

But if you start saving much later, you’ll need to set aside more to hit that comfortable mid-60 retirement mark.

Hope to retire before your 60s?

Consider saving 40-50% (or more if possible.)

5. Rebalance Asset Allocation

By now, you know that the closer you get to retirement, the warier of risk you should become when mapping out your portfolio.

Figuring out the right asset allocation will depend on a few factors. So consider how diversifying your portfolio can cushion potential risk.

Aim to invest in a diverse mix of asset class options, including bonds, stocks, cash, and other alternatives.

Review and rebalance your asset allocation yearly, so it’s more tailored to your risk tolerance and time frame.

6. Create an Estate Plan

An estate plan is something that easily gets overlooked. This includes creating or updating a will with specific information and putting your estate documents in order.

You can even set up a trust. This is a separate entity that owns your property and is managed for a beneficiary’s benefit.

Why opt for a trust?

It’s the best way to ensure your assets are distributed as per your wishes after you’re gone or unable to make financial decisions for yourself.

Also, consider opting for a life insurance plan.

Why?

A life insurance plan will ensure your loved ones are protected by the policy’s death benefits in the event of your passing.

7. Analyze Your Investments

Look at your investments with the following considerations in mind:

- Growth potential: Make sure the growth of your investment portfolio outruns inflation. But, in the process, ensure you’re not exposing your savings to significant market changes.

- Flexibility: You need to have access and control over your assets at all times. But, remember, flexibility can entail giving up a larger income portion in exchange for access. So figure out what you want based on your individual situation.

- Guaranteed income: Your investment returns will fluctuate. So consider fixed income annuities to provide a stable income for necessities during your retirement. Even a combination of annuities with other fixed income investments (thinks certificates of deposit and treasury bonds) can generate good cash flow to cover essential expenses.

Remember:

Stay updated with all investment material, financial news, and other retirement related content.

8. Get Retirement Planning Assistance From A Financial Professional

Feeling overwhelmed by the mere thought of retirement planning?

We get it — it’s a lot!

Some people are happy to put together a retirement plan independently. But others can benefit from a bit of guidance or general information about their retirement options.

That’s where a financial professional can come in.

Every 5-10 years, check in with a financial advisor to seek guidance with your investment portfolio.

Obtaining accurate information is critical.

So, do your due diligence before hiring a registered investment advisor. Make sure to:

- Check if the adviser is a member of any professional trade organization.

- Verify their credentials.

- Ask them for Part I and Part II of the Federal Securities Disclosure Form ADV. This includes their qualifications and past financial or legal problems.

There are many investment advisory services available that can help you on your retirement journey. Some include:

- Avantax Advisory Services sm

- Avantax Wealth Management sm, member FINRA SIPC

- LPL Financial, member FINRA SIPC

One more thing:

You may need legal advice or specific information on taxes as you plan your retirement living.

So if you have any doubts, always consult legal or tax professionals.

Ready To Make The Most Rewarding Investments For Your Retirement?

A solid retirement strategy doesn’t have to be a dreary task.

While it’s a lot of pressure to plan for the unknown, work on it step-by-step.

Just start by calculating when you hope to retire and how much money you’d need to live comfortably. And, if you need help, speak to a registered investment advisor and legal or tax professionals.

Meanwhile, if you’d like to add a long-term investment option like fine wine to your portfolio, check out the Vinovest website.